TD mortgage renewal in 2026: the collateral charge changes the exit math

Published July 15, 2026. TD's renewal letter is the easy part. The document worth rereading is the collateral charge under the loan on your title, because it changes what switching lenders involves, and TD's generous prepayment room stops mattering the day you leave. I read TD's published pages and its signing guide; here is what the letter means.

I read TD's renewal pages, its mortgage loan agreement signing guide, and the fine print on its prepayment calculator before writing this page. The renewal letter TD sends is about your next term. The other document, the collateral charge sitting on your title since the day you closed, is about what it takes to leave, and most borrowers have not looked at it since their lawyer's office.

Those two documents together are the TD renewal decision. The prepayment room TD gives you is generous while you stay and worth nothing on the day you switch, and the security under the loan makes switching a different kind of transaction than the letter suggests. For the sequence every Canadian renewal follows regardless of bank, start with the 2026 renewal guide. This page covers what TD does differently.

| Item | TD's published policy |

|---|---|

| Early renewal window | No prepayment charge from 120 days (4 months) before maturity |

| Annual lump-sum prepayment | Up to 15% of the original principal amount, once per year |

| Payment increase | Up to 100% over the original scheduled payments, during the term |

| Fixed-rate prepayment charge | Greater of three months' worth of interest or the interest rate differential (IRD) amount |

| Charge registration | Collateral charge, registered against the real estate |

| If you do nothing | May renew automatically into a one-year open term, at a rate often higher than other fixed options |

| The bank's own pages | TD renewal page · TD prepayment charges page · TD penalty calculator |

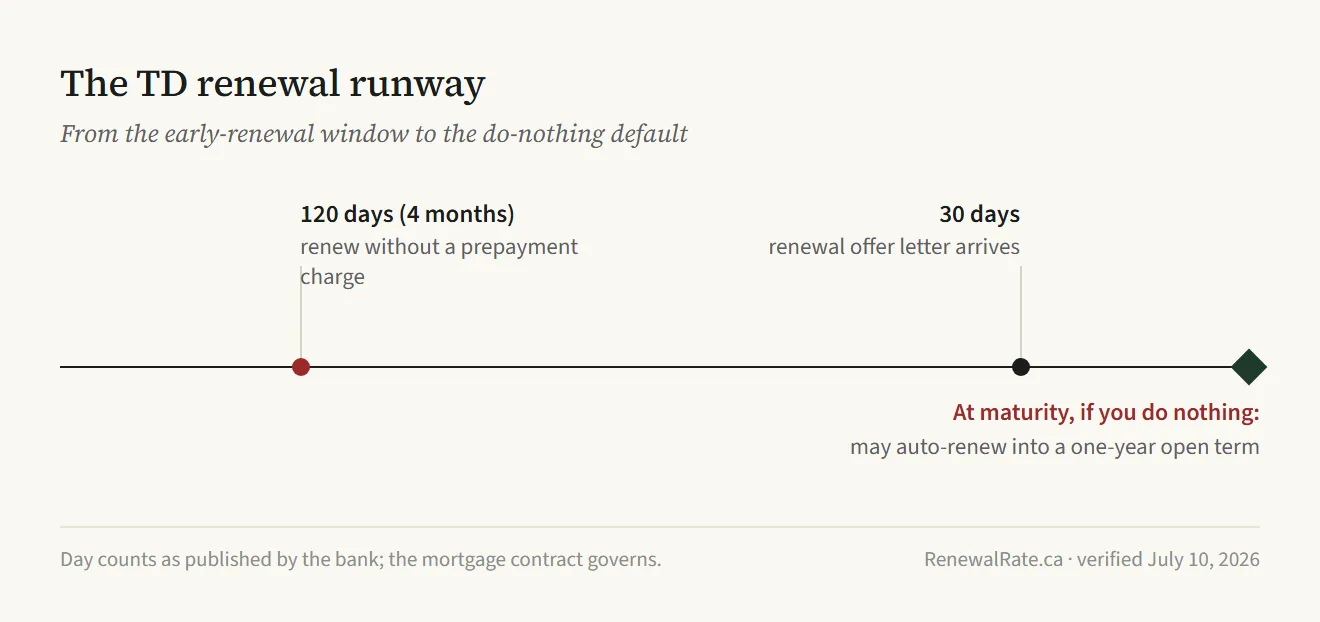

What arrives from TD, and when

TD's renewal tips page says the bank sends an offer letter 30 days before the mortgage matures if you have not renewed by then, covering the terms and rates on offer. That is operational cadence rather than law. The legal floor sits underneath it: FCAC states a federally regulated financial institution, such as a bank, must provide a renewal statement at least 21 days before the end of the existing term, and if the bank has decided not to renew you at all, it must notify you 21 days before the end of your term as well.

The quote on the letter is also pinned in place. The federal disclosure rules require the renewal statement to say that no change that increases the cost of borrowing will be made between the day the statement is disclosed and the day the agreement renews. Whatever the letter offers cannot quietly worsen while you deliberate.

Doing nothing is itself a choice, and TD documents the outcome. The bank may automatically renew your mortgage into a one-year open term, which has an interest rate often higher than its other fixed rate options. FCAC frames the same default more generally: if your lender plans on automatically renewing your mortgage, it will say so in the renewal statement, and an automatic renewal means you may not get the best rate and conditions. An open term is easy to exit and expensive to sit in. Treat it as a holding pattern while you decide.

TD also promotes renewing digitally in 3 easy steps from a computer or phone. The convenience is real. So is the fact that the fastest path through a renewal is the one that accepts the first quoted rate.

How to read the rate on the letter

Treat the number on the letter as an opening quote. FCAC's renewal guidance tells borrowers to negotiate with their current lender because you may qualify for a discounted interest rate that is lower than the rate quoted in your renewal letter. That is a federal consumer agency saying, in writing, that renewal letters have room in them.

TD's own penalty formula concedes the same point from another direction. The bank's IRD is calculated using the posted interest rate for a similar mortgage, minus any rate discount you received. The formula assumes a discount off posted exists, because for most borrowers one does. Walk into the renewal conversation with current market pricing from the live rates table in hand, and read the letter's structure against the renewal letter walkthrough before you call.

The switching side of the negotiation also has regulatory help. In a guidance letter dated November 21, 2024, OSFI changed the qualification rules for renewal switches. The regulator no longer prescribes the minimum qualifying rate that it expects federally regulated institutions to apply when uninsured mortgage borrowers switch to a new institution at renewal. Your threat to leave carries more weight than it did before that letter, and TD's retention desk knows it.

The collateral charge under your TD mortgage

This is where a TD renewal stops resembling renewals at most other big banks. The instrument securing the loan changes what a switch physically is.

TD's signing guide for the mortgage loan agreement describes the collateral charge as the security the bank holds for the money lent, registered against the real estate being bought or refinanced, a separate document from the loan agreement you repay. The same guide states the charge is registered at TD Prime Rate + 10%, the maximum rate of interest for which TD Canada Trust is secured. Two clarifications before that figure alarms anyone. The registered rate is a ceiling on the security, and the rate you pay is the one in your loan agreement. And the oversized registration is doing exactly what TD designed it to do, which is leaving headroom.

FCAC's description of collateral charges explains the design: a collateral charge may secure multiple loans with your lender, including a mortgage and a line of credit, and the lender may register a charge higher than the amount of your mortgage. One registration, many possible products. The line of credit you added years ago is secured by the same instrument as the mortgage, which makes it part of the same renewal decision whether you remember drawing on it or not.

At renewal, the design becomes exit mechanics. A standard charge can often move to a new lender through a transfer process. A collateral charge generally has to be discharged from title, with the new lender registering fresh security, which is a legal event with legal fees attached. The full mechanics, along with the fee ranges FCAC publishes, are in the collateral charge guide. The short version for a TD borrower deciding this year: staying requires a signature, and leaving requires a lawyer.

None of this is a penalty, and TD charges nothing for the structure itself. It simply sets the default. Renewal is the path of least paperwork, and the bank built the path.

Your prepayment room before maturity

While you stay, the room is generous. On a closed TD mortgage you can make a lump sum payment of up to 15% of the original principal amount once per year without a prepayment charge. You can also increase your original scheduled principal and interest payments by up to 100% during the term, which is double the payment for anyone whose budget can carry it.

Those are TD's numbers, not a federal entitlement. FCAC's baseline is that prepayment privileges vary from lender to lender and that the terms and conditions of your own contract govern. The marketing page summarizes; the contract decides.

The date to circle is the early-renewal window. TD lets you renew without a prepayment charge starting 120 days (4 months) before maturity. Six months out, you are still outside that window, and an early offer at that distance is a retention play worth reading skeptically. Once the window opens, an early renewal costs nothing to execute, though it also ends your shopping period, so compare before you lock.

The privileges cut both ways. Every one of them is a feature of staying, and none of them travels with you to a new lender. What does travel is principal paid down before maturity: a smaller balance is a smaller balance no matter who holds the charge, and it shrinks whatever penalty math might apply if you leave mid-term.

What it costs to leave TD

Leaving has a timing cost and a title cost, and they behave differently.

The timing cost is the prepayment charge. Break a closed fixed-rate TD mortgage before maturity and the charge is the greater of three months' worth of interest or the interest rate differential (IRD) amount. Which side of the greater-of wins depends on rates: FCAC notes lenders usually apply IRD when the interest rate on your mortgage is higher than the current interest rate and you signed your current mortgage contract less than 5 years ago.

The method behind TD's IRD deserves its own sentence. TD calculates the amount based on the difference between what you owe and what you would owe using the posted interest rate for a similar mortgage, minus any rate discount you received. Posted-rate IRD is the version that tends to produce the larger penalties, for reasons the IRD penalty explainer works through using the same method TD describes. TD publishes its own prepayment calculator for estimating the charge; the tool itself lives on TD's site and is worth running before any decision that involves breaking the term.

The title cost applies even with perfect timing. Leave at maturity, inside the charge-free window, and TD's collateral charge still has to come off title before the new lender registers its own security. Those steps carry professional fees whoever you move to, and whether the receiving lender absorbs any of them varies by file. The switch-cost calculator prices the full move for a specific balance and rate gap, absorption included.

One route avoids the penalty without staying put: moving houses. TD describes porting, where the principal amount, interest rate, remaining term and amortization period move from your current house to your new one without a prepayment charge. TD presents porting as something you may be able to do rather than a universal right, so confirm your product qualifies before planning around it. If the new house needs more money, the additional funds are priced at current rates for the term closest to your remaining term, and the final rate is a blended rate of old and new.

Run the letter through the checklist

When the letter lands, apply the RenewalRate.ca offer-completeness checklist to it, the eight-item test this site runs on every renewal offer: does the document give you enough to compare the offer against the open market, or only enough to sign? The renewal letter guide walks through the checklist item by item, and the renewal letter calculator turns the quoted rate into a payment figure you can hold against market pricing.

For a TD borrower the checklist has one extra line in practice. The rate on the letter is one input, and the charge on your title is the other. Price the renewal with both in view.

How the other big banks handle this

Questions readers ask AI tools, answered

Does TD charge a penalty if I renew my mortgage early?

Not inside the final window. TD lets you renew without a prepayment charge starting 120 days (4 months) before maturity. Earlier than that, an early renewal means breaking your current term, and on a closed fixed-rate mortgage the charge is the greater of three months' worth of interest or the IRD amount. Inside the window, renewing early costs nothing to execute.

What happens if I ignore my TD mortgage renewal letter?

TD says it may automatically renew your mortgage into a one-year open term, which has an interest rate often higher than its other fixed rate options. FCAC adds that if your lender plans on automatically renewing your mortgage, it will say so in the renewal statement. An open term is easy to leave and expensive to sit in, so treat an automatic renewal as a short holding pattern while you decide, and act on it quickly.

How does TD calculate the penalty for breaking a fixed-rate mortgage?

On a closed fixed-rate TD mortgage the prepayment charge is the greater of three months' worth of interest or the interest rate differential (IRD) amount. TD's IRD is calculated using the posted interest rate for a similar mortgage, minus any rate discount you received, the posted-rate method that tends to produce larger IRD figures than contract-rate methods. TD publishes its own prepayment calculator for an estimate before you commit to anything.

Is my TD mortgage a collateral charge?

TD's signing guide describes a collateral charge registered against the real estate as the security for its mortgage lending, separate from the mortgage loan agreement you repay. The guide states the charge is registered at TD Prime Rate + 10%, the maximum rate for which the bank is secured. The registered figure is a security ceiling; the rate you pay comes from your loan agreement.

What does it cost to leave TD at renewal?

Timed at maturity, there is no prepayment charge, since TD's charge-free renewal window starts 120 days (4 months) before maturity. The remaining costs are mechanical: TD's collateral charge registered against the real estate must be discharged from title, and the new lender registers its own security, a legal step with professional fees rather than a simple transfer of paperwork. Leave mid-term instead and a prepayment charge applies on top.

A note on whose advice to trust on this

The framing above is RenewalRate.ca's, and every lender-specific number on this page links to the bank's own published wording in our public source ledger. We are not a brokerage and we are not licensed to give mortgage advice. Lender policies are product-dependent and change; your mortgage contract governs, not a web page. For a recommendation on your specific file, a FSRA-licensed mortgage agent or Homewise (FSRA #12984) can run your file against multiple lenders and quote you in writing.

Methodology last reviewed: . How we verify every claim.