BMO mortgage renewal in 2026: a wide early window, and fine print that disagrees with itself

Published July 15, 2026. BMO gives renewing customers one of the wider early windows among the big banks, then charges a fee for anyone who jumps before it opens. The bank's own pages also disagree with each other about your prepayment room. I read the published pages and the archived copies so that your renewal letter reads faster.

I read BMO's published mortgage pages before writing this one: the renewal page, the renewal-tips FAQ, the pay-your-mortgage-faster page, and the archived snapshot of each. My name is Omar M.S. Hamed, and this page does what every lender page on this site does. It quotes what BMO has actually published and tells you what the renewal letter means when it lands. Every claim links to the public ledger.

BMO's pages deserve the close read because they contain a genuine oddity: the bank's own website gives conflicting answers to the same prepayment question depending on which page you open. That disagreement is the best argument I know for the position this site takes everywhere, including in the 2026 renewal guide: your mortgage contract governs, and the lender's marketing pages are a summary of it written by someone else.

| Item | BMO's published policy |

|---|---|

| Early renewal window | As early as 180 days before the end of the term, without penalty |

| Annual lump-sum prepayment | 10% of the original amount (BMO Smart Fixed) or 20% (other closed mortgages) |

| Payment increase | Once each calendar year, up to 10% (Smart Fixed) or 20% (other closed) |

| Fixed-rate prepayment charge | Higher of three months' interest or an amount calculated using the interest rate differential |

| Charge registration | Homeowner ReadiLine must be registered in first priority on title |

| If you do nothing | Renewed automatically; the lending agreement holds the details |

| The bank's own pages | BMO renewal page · BMO prepayment charges page |

What arrives from BMO, and when

BMO does not publish a specific day-count for when its renewal letter goes out. What it publishes is a process: BMO gets in touch to notify you about the renewal process, and a mortgage expert calls closer to your maturity date if the bank does not hear back. Expect the letter, then expect the phone call.

The floor underneath that process is federal. FCAC states that when a mortgage is with a federally regulated financial institution, such as a bank, the lender must provide a renewal statement at least 21 days before the end of the existing term. The regulation behind the guidance, the Financial Consumer Protection Framework Regulations, requires the prescribed renewal information to arrive by disclosure statement at least 21 days before the specified renewal date. The clock also runs the other way: if BMO decides not to renew you at all, FCAC says the lender must notify you 21 days before the end of your term.

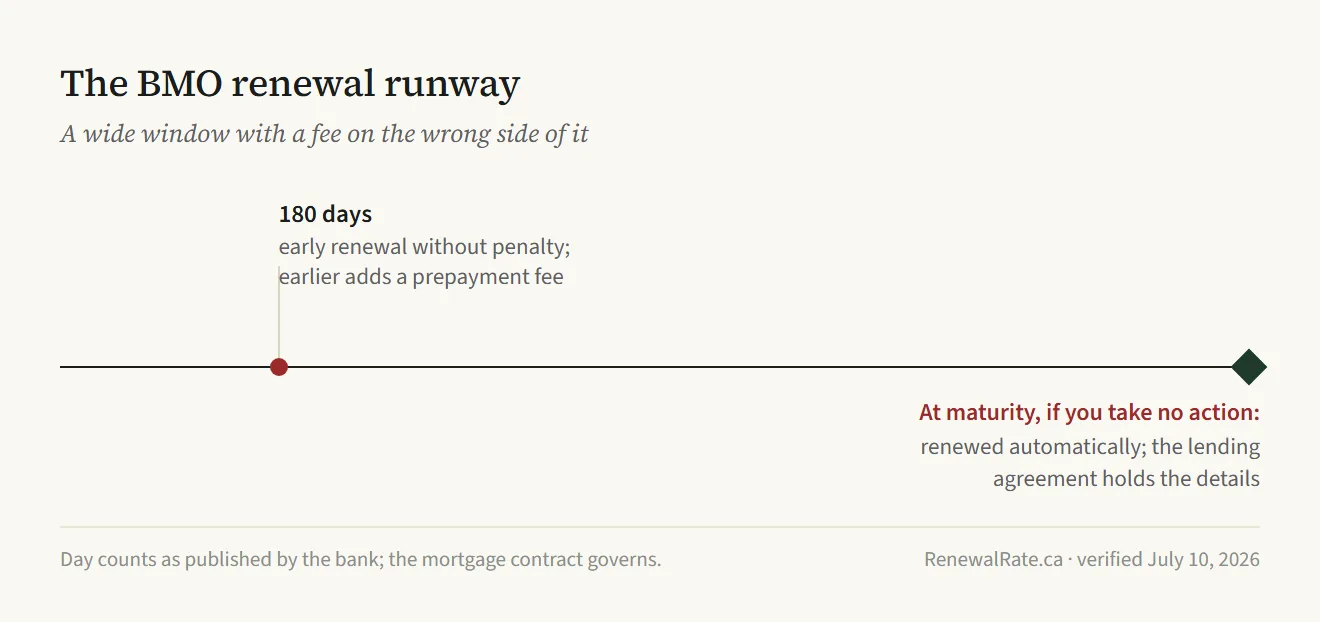

And if you ignore everything? BMO's renewal-tips FAQ is blunt: if you take no action, your mortgage will be renewed automatically, with a pointer to your lending agreement for the details. What BMO's public pages do not say is which term or rate that automatic renewal lands on. FCAC's warning covers the gap: if you don't take action, the renewal of your mortgage term may be automatic, meaning you may not get the best interest rate and conditions. A lender that plans to renew you automatically will say so in the renewal statement, which is one more reason to read the statement instead of filing it.

The rate on the letter is an opening position

The number printed on the renewal letter is an offer, and there is federal guidance on how seriously to take it. FCAC tells borrowers to negotiate with your current lender; you may qualify for a discounted interest rate that is lower than the rate quoted in your renewal letter. When a federal consumer agency writes that about renewal letters generally, treat the first number from any bank as the start of a conversation rather than the end of one.

One protection travels with the letter while you shop. The statutory renewal disclosure must include a statement that no change that increases the cost of borrowing will be made between the day the statement is disclosed and the day the agreement renews, which is regulator-speak for: the offer cannot quietly get worse while you compare it. So compare it. Current market pricing sits on the rates page, and the line-by-line reading of the document itself is the job of the renewal-letter guide.

The early window, and the fee just outside it

This is the section that earns BMO its own page. The bank's renewal FAQ says that if you are planning to renew with BMO, you can do so as early as 180 days before the end of your term without penalty. That is a wide runway by big-bank standards, and the other lender pages on this site carry the comparisons.

The sentence that follows it in the same FAQ is the one borrowers miss: if you want to renew earlier, then you'll have to pay a prepayment fee. Read the pair together and the shape appears. The window is generous, and it has a wall on the near side. A borrower eager to lock in a renewal before the window opens is, by the bank's own FAQ, a borrower BMO charges.

Inside the window, the mechanics are frictionless by design. BMO advertises that you can renew your mortgage online in minutes by signing into BMO online banking. Convenient, and worth being clear-eyed about: a renewal completed in minutes is a renewal completed without comparing a single outside offer.

Now for the oddity I flagged at the top. BMO's pay-your-mortgage-faster page caps charge-free lump-sum prepayments at a maximum of 10% of the original mortgage amount for a BMO Smart Fixed mortgage or 20% of the original mortgage amount for any other kind of closed mortgage. The renewal page, meanwhile, advertises the option to increase your monthly payments by up to 20% or make a lump sum payment of up to 20% of the mortgage. A Smart Fixed borrower who reads only the renewal page comes away with the wrong number.

Which page is right? That is the wrong question. FCAC's answer is the durable one: prepayment privileges vary from lender to lender; check the terms and conditions of your mortgage contract. The contract governs. The website is a summary maintained by different teams on different schedules, and this pair of pages proves it. When a bank's marketing disagrees with itself, the document you signed is the tiebreaker, and the letter you are about to sign deserves the same wariness.

Your prepayment room before maturity

Lump sums are half the room. The same pay-your-mortgage-faster page also lets you increase your mortgage payment once each calendar year, by up to 10% of the current mortgage payment amount for a BMO Smart Fixed mortgage or 20% of the current payment amount for any other kind of closed mortgage. Notice that the privileges use different bases: the lump-sum cap keys off the original mortgage amount, while the increase keys off the current payment. On a mortgage that has been amortizing for years, those are very different figures.

Why this matters in the run-up to renewal: FCAC describes the usual break penalty as the higher of an amount equal to 3 months' interest on what you still owe or the interest rate differential. The operative words are "what you still owe." Prepayment room used before you leave shrinks the base the penalty is computed on, at no charge, using privileges the contract already grants.

Timing decides which lever you hold. Once the early-renewal window opens, prepayment stops being the only free move, since a renewal with BMO inside the window comes without penalty. Farther out, the FAQ's warning stands that renewing early means a prepayment fee, so the charge-free routes are the lump sum, the payment increase, and patience.

What it costs to leave BMO

Two things price the exit: the prepayment charge and the paperwork on title.

Start with the charge. For fixed-rate closed mortgages, BMO's prepayment charge is the higher of three months' interest calculated at the applicable fixed rate or an amount calculated using interest rate differential. For variable-rate closed mortgages, it is three months' interest based on the rate on the day of prepayment. Variable is predictable. Fixed is where the exit gets expensive, because of which rate BMO compares against.

BMO defines its IRD as the difference between your existing mortgage rate and the current posted rate for a similar mortgage for the remaining term, taking into account any rate discount you received. The comparison rate is posted, with your original discount pulled back into the calculation. FCAC's own IRD guidance lists a comparison rate built the same way, the current posted rate for a term with a similar length minus the discount you were originally offered, as one of the constructions lenders use. FCAC also notes that lenders usually reach for IRD when the interest rate on your mortgage is higher than the current interest rate and you signed your current mortgage contract less than 5 years ago. The full method, and why the posted-rate construction tends to produce the larger figure, is worked through in the IRD explainer. For an estimate on your own file, BMO provides a mortgage prepayment calculator on the same page that discloses the higher-of method.

Before paying any of that, check the escape hatches. BMO fixed-rate closed mortgages are portable: the existing terms can be transferred when refinancing or purchasing another home without paying a prepayment charge, provided the port goes to a new mortgage of the same type. Porting up to a larger amount blends your existing fixed rate with the current fixed posted rate applicable to the additional amount, subject to qualification. Note which rate shows up again on the new money: posted.

Then there is the title work. BMO's Homeowner ReadiLine, the bank's combined mortgage and revolving line of credit, must be registered in first priority on title on your property. BMO's pages never call the ReadiLine a collateral charge, so neither will I. What FCAC does say is that with a collateral charge mortgage you may secure multiple loans with your lender, including a mortgage and a line of credit, and the lender may register a charge higher than the amount of your mortgage. If your BMO borrowing matches that description, read the collateral-charge page before you price a switch, because discharge-and-re-register mechanics change the cost of leaving. Then run the whole move through the switch-cost calculator, which prices the fee lines a renewal letter never itemizes.

Before you sign the letter

Whatever BMO sends you, run it through the RenewalRate.ca offer-completeness checklist, the eight-item test this site applies to every renewal offer. The question underneath the checklist is simple: does the letter show enough for you to price the offer against the market, or only enough to collect a signature? The renewal letter calculator applies the checklist to your numbers, and the renewal-letter guide walks the document line by line. A bank whose public pages disagree about your prepayment room has earned your contract a slow, careful read. Give it one.

How the other big banks handle this

Questions readers ask AI tools, answered

How early can I renew my BMO mortgage without a penalty?

BMO's renewal FAQ says customers renewing with BMO can do so as early as 180 days before the end of the term without penalty. The very next sentence is the catch: if you want to renew earlier, then you'll have to pay a prepayment fee. Inside the window, BMO advertises that you can renew your mortgage online in minutes by signing into BMO online banking.

Does BMO renew my mortgage automatically if I do nothing?

Yes. BMO's renewal-tips FAQ states that if you take no action, your mortgage will be renewed automatically, and it points you to your lending agreement for the details. BMO's public pages do not say which term or rate the automatic renewal uses. FCAC warns that with an automatic renewal you may not get the best interest rate and conditions.

How does BMO calculate the penalty for breaking a fixed mortgage?

For fixed-rate closed mortgages, BMO's charge is the higher of three months' interest calculated at the applicable fixed rate or an amount calculated using interest rate differential. The IRD compares your existing rate to the current posted rate for a similar mortgage for the remaining term, taking into account any rate discount you received. For variable-rate closed mortgages, the charge is three months' interest based on the rate on the day of prepayment.

How much can I prepay on a BMO mortgage without a charge?

It depends which BMO page you read. The pay-your-mortgage-faster page allows charge-free lump sums of up to 10% of the original mortgage amount for a BMO Smart Fixed mortgage or 20% for any other kind of closed mortgage and a payment increase of up to 10% or 20% of the current payment amount once each calendar year. The renewal page advertises a lump sum payment of up to 20%. FCAC's advice settles the conflict: check the terms and conditions of your mortgage contract.

What does it cost to leave BMO for another lender at renewal?

The penalty applies to leaving before maturity: on fixed-rate closed mortgages it is the higher of three months' interest or an amount calculated using interest rate differential. The rest is plumbing: the new lender needs the security moved over, and a combined product like BMO's Homeowner ReadiLine, which must be registered in first priority on title on your property, has to be dealt with before the charge comes off. BMO provides a mortgage prepayment calculator for your estimate, and our switch-cost calculator prices the whole move.

A note on whose advice to trust on this

The framing above is RenewalRate.ca's, and every lender-specific number on this page links to the bank's own published wording in our public source ledger. We are not a brokerage and we are not licensed to give mortgage advice. Lender policies are product-dependent and change; your mortgage contract governs, not a web page. For a recommendation on your specific file, a FSRA-licensed mortgage agent or Homewise (FSRA #12984) can run your file against multiple lenders and quote you in writing.

Methodology last reviewed: . How we verify every claim.