National Bank mortgage renewal in 2026: the collateral-charge bank that renews by phone

Published July 15, 2026. I read National Bank's renewal, prepayment, and All-In-One pages and pulled out what the letter commits the bank to. Most of it runs on the standard federal clock. The exception sits on your title, and it decides how expensive leaving will be.

I read National Bank's renewal page, its pay-faster page, its prepayment charges calculator, and the help centre entries most borrowers only find after the letter has already landed. Every factual claim on this page is tied to a verbatim quote in our public ledger, pulled and verified on the publication date. I am Omar M.S. Hamed, and this page reads National Bank's letter the way I read all of them: against what the bank has published, quote by quote.

Two things separate a National Bank renewal from the rest of the Big Six, and I will quote the bank on both below: who handles the renewal, and what kind of charge sits on your title. Neither appears anywhere on the renewal notice itself, and both change what the notice is worth.

| Item | National Bank's published policy |

|---|---|

| Early renewal window | Up to 4 months before the end of the term, with no penalty |

| Annual lump-sum prepayment | Up to 10% of the principal amount borrowed, without fees |

| Payment increase | An additional payment up to the regular payment amount, on each payment date |

| Fixed-rate prepayment charge | Higher of 3 months of interest, or 1 month of interest (max. $500) plus the interest differential |

| Charge registration | The collateral mortgage is the type used at National Bank |

| If you do nothing | Renewal notice arrives at least 21 days before the end of the term (no published auto-renewal default) |

| The bank's own pages | National Bank renewal page · National Bank prepayment charges page · National Bank penalty calculator |

What arrives before your term ends

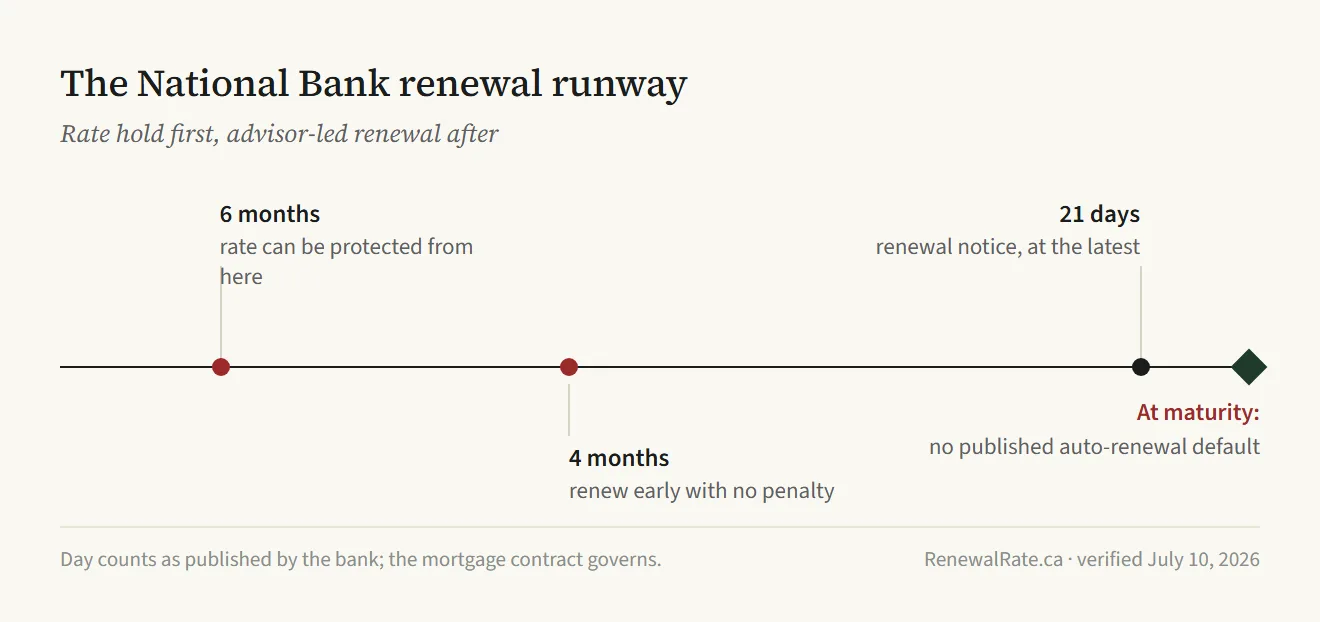

National Bank's help centre is specific: you will receive a mortgage renewal notice at least 21 days before the end of your term. That is the federal floor restated. FCAC says a lender that is a bank must provide you with a renewal statement at least 21 days before the end of the existing term, and the same clock runs in reverse: if National Bank decides it will not renew you, it must notify you 21 days before the end of your term.

The statement is worth reading for what it locks. The disclosure rules prescribe a statement that no change that increases the cost of borrowing will be made to the credit agreement between the day the statement is disclosed and the day the mortgage renews. The offer can improve after it is printed. It cannot get worse.

Doing nothing is itself a decision. FCAC's warning is that if you don't take action, the renewal of your mortgage term may be automatic, meaning you may not get the best rate and conditions, and the renewal statement will say so if auto-renewal is the plan. The wider term-end timeline lives in the 2026 renewal guide; this page stays on what National Bank specifically does.

The rate on the letter is an opening number

Nothing in the disclosure rules obliges the printed rate to be the bank's best offer, and FCAC says as much to borrowers directly: negotiate, because you may qualify for a discounted interest rate that is lower than the rate quoted in your renewal letter.

Your side of the table is stronger at National Bank than the letter implies. Renewing you costs the bank almost nothing to process: the renewal page says there is no need to complete a financing application, no request for proof of income or qualifications, and no credit bureau check. A customer the bank does not have to underwrite is a customer the bank very much wants to keep.

The switch threat behind your negotiation is also more credible than it used to be. In a guidance letter dated November 21, 2024, OSFI exempted uninsured mortgage straight switches from the prescribed minimum qualifying rate. The regulator no longer prescribes the minimum qualifying rate (MQR) that federally regulated institutions were expected to apply when uninsured borrowers switch to a new institution at renewal. Requalifying at a stress-tested rate used to keep renewers captive; a straight switch no longer carries it.

So treat the printed number as the anchor the bank chose, then check it against the live market on the rates page and against the letter's other fields with the renewal letter decoder. The person who calls you can move, and at this bank someone does call, as the next section explains.

Every mortgage here is a collateral charge, and renewal is a phone call

Most of the Big Six register a standard charge on plain mortgages and save collateral registration for products paired with credit lines; the lender pages track who does what. National Bank does not split its book. The help centre says it in a single sentence: the collateral mortgage is the type of mortgage used at National Bank. TD is the only other Big Six bank that runs collateral registration across everything it writes.

What that means, in FCAC's words: with a collateral charge you may secure multiple loans with your lender, including a mortgage and a line of credit, and the lender may register a charge higher than the amount of your mortgage. The full mechanics, including what discharge and re-registration involve when you switch, are on the collateral charge page. The renewal-day consequence compresses to one line: staying with National Bank is frictionless, and leaving is a discharge-and-reregister exercise rather than a transfer.

The All-In-One is where the charge earns its keep. National Bank's product page says your repaid principal will automatically become available on the line of credit portion of the All-In-One. Readvanceable credit is convenient early in a term and sticky by the end of it. Every dollar of principal you clear can be redrawn, and each redraw adds another balance living under the same umbrella charge. A borrower switching lenders at renewal is unwinding whatever the umbrella has accumulated, not just moving one loan. Scotiabank renewers with a STEP will recognize the shape.

Then the process quirk: there is no self-serve renewal flow to click through. National Bank does not advertise an online renewal path on nbc.ca as of this page's publication date; what its renewal page advertises is the opposite, that its advisors can complete the entire renewal process over the phone. Renewal at this bank is a conversation with a person whose job title includes the word advisor.

That cuts both ways. You cannot sleepwalk through a midnight click into a posted rate, which is genuinely protective. It also means every National Bank renewal is a live negotiation whether you prepared for one or not. The bank's staff run this call daily; you run it once every few years. Close that gap before the phone rings: have the market rate in front of you, and remember that the requalification-free renewal described above makes you cheap to keep.

Your prepayment room before maturity

FCAC's baseline on privileges is that prepayment privileges vary from lender to lender and that the mortgage contract, and only the contract, settles yours. Here is what National Bank publishes.

The annual privilege: during the same calendar year, you can repay up to 10% of the principal amount borrowed without fees. Two details in the wording deserve attention. The percentage keys off the principal amount borrowed, which is the original figure rather than whatever you owe today. And the room resets by calendar year; go past it within one and a prepayment charge applies.

The per-payment privilege: on the date of each payment, you have the option to make an additional payment equal to or less than your regular payment, principal and interest included. That is National Bank's version of a double-up.

Then the window before maturity, which is generous on paper. National Bank lets you protect your rate from 6 months before the end of your term. It also lets you renew early, up to 4 months before the end of your term, with no penalty.

Read those as different tools. The rate hold is an option: it caps the downside while you shop, and asking for it commits you to nothing. The early renewal is an exercise: it closes the old term and starts the new one, so the comparison work has to happen before you take it, because the negotiation you skipped does not reopen afterward. Locked in early at a rate you never tested is the quiet version of auto-renewal.

What it costs to leave

Leave mid-term and the prepayment charge applies. National Bank publishes the method in its fees table: on a fixed-rate loan the charge is the higher of 3 months of interest, or 1 month of interest (max. $500) plus the interest differential, and on a variable-rate loan it is 3 months of interest. Read the fixed-rate wording closely, because the 1 month of interest (max. $500) rider stacks on top of the differential leg, a construction most other big-bank penalty tables word differently.

This is the standard industry shape with a house accent. FCAC describes the norm as usually the higher of an amount equal to 3 months' interest on what you still owe or the interest rate differential. Lenders usually use the IRD calculation when the interest rate on your mortgage is higher than the current interest rate and you signed your current mortgage contract less than 5 years ago, which describes plenty of borrowers who took a fixed rate near the recent peak.

The differential is where posted rates do their work. National Bank's own prepayment calculator asks for the posted rate from your loan agreement, and where a discount was granted, the posted rate stated before the reduction. FCAC's description of the method includes a comparison leg built on the current posted rate for a term with a similar length minus the discount you were originally offered. Posted in, posted out; the discount you negotiated years ago becomes an input to the penalty for leaving. The full mechanics, and the levers that shrink the number, are in the IRD penalty explainer.

Estimate before deciding anything. National Bank's prepayment charges calculator provides an estimate of the charges payable following a prepayment of your mortgage loan, and FCAC confirms this is standard equipment: federally regulated financial institutions, like banks, have a prepayment penalty calculator on their website.

At maturity the penalty leg falls away and the title work remains. Because the charge is collateral, the exit is a discharge and a fresh registration with the receiving lender rather than a transfer, with the fee mechanics covered on the collateral charge page. And if a sale is what ends the mortgage, National Bank's stated options are to transfer or break your mortgage, with a possible penalty for early payment. Whether the whole exercise clears the rate savings is a job for the switch-cost calculator, which runs it against your numbers.

Hold the letter against the checklist

When the notice arrives, run it through the RenewalRate.ca offer-completeness checklist, the eight-item test we apply to every renewal offer on this site. A National Bank letter that shows a rate and a signature line but stays silent on the penalty method or the charge type is an incomplete offer, and the useful response to an incomplete offer is a list of questions for the advisor who calls. The renewal letter calculator prices the offer against the current market, and the letter decoder walks each field, checklist included. Bring both to the phone call. The advisor will have their numbers ready; there is no reason yours should not be.

How the other big banks handle this

Questions readers ask AI tools, answered

Does National Bank charge a penalty if I renew my mortgage early?

Not inside the published window. National Bank lets you renew early, up to 4 months before the end of your term, with no penalty. Separately, you can protect your rate from 6 months before the end of your term, which holds a rate while you keep comparing. Breaking the term before that window is a prepayment, and the prepayment charge applies.

Is every National Bank mortgage a collateral charge?

Yes, by the bank's own description: the collateral mortgage is the type of mortgage used at National Bank. FCAC explains what that structure does: with a collateral charge you may secure multiple loans with your lender, including a mortgage and a line of credit, and the lender may register a charge higher than the amount of your mortgage. Convenient while you stay; extra title work when you leave.

How does National Bank calculate its mortgage prepayment penalty?

National Bank's fees table sets the charge at the higher of 3 months of interest or 1 month of interest (max. $500) plus the interest differential on a fixed-rate loan, and 3 months of interest on a variable-rate loan. The differential runs on posted rates: the bank's calculator asks for the posted rate stated before the reduction when a discount was granted, which is what makes fixed-rate penalties swell.

Do I have to requalify to renew my mortgage with National Bank?

No. National Bank's renewal page states there is no need to complete a financing application, and that the bank won't ask for proof of income or qualifications, or consult your credit bureau. The process is advisor-led: advisors can complete the entire renewal process over the phone. Remember the asymmetry when the call comes, because a renewal the bank does not have to underwrite is a cheap customer to keep.

What does it cost to leave National Bank at mortgage renewal?

The dollar figure depends on your file, but the mechanics are fixed. Because the collateral mortgage is the type of mortgage used at National Bank, switching means discharging the existing charge and having the receiving lender register a new one, professional fees included, rather than a lighter transfer. Break mid-term and the prepayment charge applies on top; the bank's own calculator provides an estimate of the charges payable following a prepayment.

A note on whose advice to trust on this

The framing above is RenewalRate.ca's, and every lender-specific number on this page links to the bank's own published wording in our public source ledger. We are not a brokerage and we are not licensed to give mortgage advice. Lender policies are product-dependent and change; your mortgage contract governs, not a web page. For a recommendation on your specific file, a FSRA-licensed mortgage agent or Homewise (FSRA #12984) can run your file against multiple lenders and quote you in writing.

Methodology last reviewed: . How we verify every claim.