CIBC mortgage renewal in 2026: the one open day most borrowers miss

Published July 15, 2026. I read CIBC's renewal and prepayment pages line by line, plus the fine print on its mortgage-security disclosures. Two mechanics stood out: an early-renewal window that opens far sooner than most holders realize, and exactly one day in the life of every CIBC mortgage when leaving carries no prepayment charge. Most people renew straight past both.

I read CIBC's published renewal, prepayment, mortgage-security and porting pages for this piece, along with the federal disclosure rules that sit underneath them. Every number below comes from one of those documents, and every one links to our public ledger, where you can read the exact sentence CIBC or the regulator wrote and decide whether my reading of it holds up.

Two mechanics organize everything that follows. CIBC opens its early-renewal window unusually far from maturity, and it states in writing that every one of its mortgages becomes fully open on the day the term ends. The renewal letter is drafted on the quiet assumption that you will notice neither. This page is the opposite assumption.

| Item | CIBC's published policy |

|---|---|

| Early renewal window | As early as 150 days before maturity, subject to qualifying |

| Annual lump-sum prepayment | 10%, 15% or 20% annually, depending on the product |

| Payment increase | Up to 100% of the original regular payment, at any time in the term |

| Fixed-rate prepayment charge | Greater of two amounts, starting with 3 months' interest on the amount prepaid |

| Charge registration | Standard charge registered for the exact amount borrowed |

| At maturity | Every CIBC mortgage becomes open at the end of the term |

| The bank's own pages | CIBC renewal page · CIBC prepayment charges page · CIBC penalty calculator |

What arrives from CIBC and when

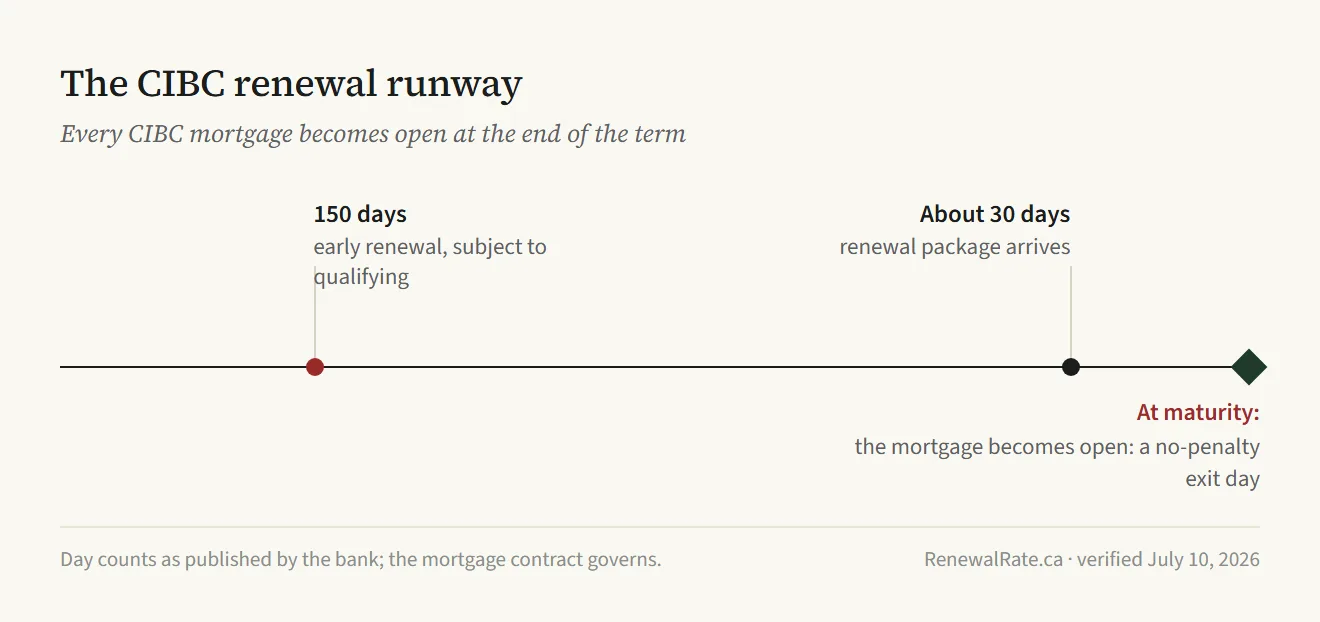

The paperwork is a renewal package with the bank's offer inside. Per its renewal resource page, CIBC sends out renewal offers about 30 days before the mortgage maturity date. The bank's FAQ describes what's inside: the package includes mortgage product offers and terms, among other options.

The legal floor sits just underneath that timing. FCAC states that a federally regulated financial institution must provide you with a renewal statement at least 21 days before the end of the existing term. Run the subtraction yourself and notice how little daylight separates CIBC's stated practice from the statutory minimum. Waiting for the envelope is not a plan.

Two more federal rules shape the do-nothing path. If CIBC will not renew you, FCAC says the lender must notify you 21 days before the end of your term. If you take no action at all, FCAC warns that the renewal of your mortgage term may be automatic, meaning you may not get the best interest rate and conditions, and if your lender plans on automatically renewing it will say so in the renewal statement. Auto-renewal is the default outcome, and it is priced like a default outcome.

One line item you can cross off: CIBC doesn't charge any administrative fees for renewing a mortgage. Signing the enclosed offer costs nothing, which is exactly what makes the path of least resistance so well paved.

Is the rate on the letter negotiable?

Treat the printed rate as an opening position. Canadian banks maintain posted rates and then discount from them, and a renewal letter is a first quote from a party that would prefer you not to shop. Nothing about that is unique to CIBC; it is how the category works.

The regulator says as much. FCAC's renewal guidance tells borrowers to negotiate with your current lender, because you may qualify for a discounted interest rate that is lower than the rate quoted in your renewal letter. That sentence sits on a Government of Canada page, which is a useful thing to remember mid-phone-call.

A statutory backstop protects you while you shop. The renewal disclosure must include a statement that no change that increases the cost of borrowing will be made between the day the statement is disclosed and the day the credit agreement is renewed. The offer in your hands cannot quietly get worse while you compare it against the current market. So compare it. For help reading the rest of the document, the renewal letter guide walks it line by line.

The one day your CIBC mortgage is fully open

The most useful sentence CIBC publishes about renewal sits on its prepayment page, well away from the renewal marketing. All CIBC mortgages become open at the end of the mortgage term, and you can pay as much as you want on your mortgage before you renew.

Read that as a mechanic, and a valuable one. An open mortgage can be paid down or paid out without prepayment charges, and CIBC is saying every one of its mortgages passes through that state at maturity. On any other day of a closed term, leaving triggers the penalty math in section five. On maturity day there is no penalty math to do.

The practical use is timing. If you are switching lenders, aim the new lender's funding date at the maturity date, because a discharge that funds on maturity day pays out a fully open balance, while one that funds weeks early pays out a closed one and gets billed accordingly. If you have cash earmarked for the mortgage, the same day is the moment it can go in without consuming any privilege room.

Now the complication, because CIBC has a structural one. The bank's flagship combined product is the Home Power Plan, which CIBC describes as an all-in-one mortgage and line of credit where the line of credit automatically increases as you pay down your mortgage. Readvanceable credit is genuinely convenient. It is also registered against your title differently.

For the Home Power Plan, CIBC typically registers the charge for up to 100% of the property value, so borrowing 80% of your home's value can still mean a charge registered for 100% (or more). That is a collateral charge. FCAC's description of the structure: with a collateral charge mortgage you may secure multiple loans with your lender, including a mortgage and a line of credit, and the lender may register a charge higher than the amount of your mortgage.

The maturity-day opening removes the prepayment charge. It does not remove the registration. A Home Power Plan holder who wants to leave is discharging a collateral charge and everything secured under it, a heavier process than moving a standard charge between lenders, and I wrote up what that process involves and costs in the collateral charge guide. If your CIBC mortgage came bundled with a credit line, read that before you price a switch.

The contrast with CIBC's plain mortgages is documented by the bank itself, which is unusual and to its credit: CIBC registers the standard charge for the exact amount you borrow. Plain-mortgage holders keep the cleaner exit. Home Power Plan holders traded it for the readvancing line, whether or not anyone framed that as a trade at signing.

Your prepayment room before maturity

Until maturity day, closed-mortgage rules apply, and CIBC's prepayment room depends on which product you hold. The bank allows an annual lump-sum prepayment of 10%, 15% or 20% depending on your product, and to avoid prepayment charges the payment cannot exceed your allowable prepayment privilege.

Which figure is yours is a contract question, and the spread is not trivial. CIBC's fixed-rate closed mortgage carries terms of up to 10 years and allows prepayment of up to 10% annually, the bottom of the bank's own range.

A second lever runs alongside the lump sum: CIBC lets you increase your payment amount up to 100% of the original regular payment at any time over the mortgage term. Payment increases are the quieter privilege, and the one renewal letters never remind you about.

None of this is standardized across lenders. FCAC's baseline is that prepayment privileges vary from lender to lender, and borrowers should check the terms and conditions of their mortgage contract. Your contract wording outranks this page and anything a chatbot told you this morning.

Then there is the early-renewal window, the piece CIBC advertises least and rewards most. The bank says you may qualify to renew your mortgage as early as 150 days before maturity. Note the verb: qualify is CIBC's call, and the terms depend on your file. The window still matters, because it opens months before the letter arrives. If rates are falling, you can let it pass. If they are rising, or you simply want the decision made, early renewal moves the negotiation onto your calendar instead of the bank's. The wider timeline, including what to do at each distance from maturity, is in the 2026 renewal guide; how other banks' windows compare is on the lender pages.

What it costs to leave CIBC

Break a fixed-rate closed CIBC mortgage before maturity and the bank's own calculator page states the method: for most fixed-rate closed mortgages, the prepayment charge is usually 3 months' interest or the IRD, whichever is greater.

The IRD leg is where penalties grow. CIBC calculates it as interest over the remaining term of your mortgage, calculated at CIBC's current posted interest rate for the comparison mortgage identified in your mortgage documents. The operative word is posted. The bank's penalty calculator confirms the same choice of rate: the comparison rate is based on CIBC's current posted rate for a mortgage with a term that's similar to the remaining term on your mortgage. What the posted-versus-discounted distinction does to a penalty is the subject of the IRD explainer, which walks the calculation in full.

Variable is simpler, with its own catch. For a variable-rate closed mortgage, the charge is 3 months' interest on the amount you prepay, calculated at the CIBC prime rate. Notice which rate the interest is calculated at.

None of this is CIBC inventing something exotic. FCAC says the prepayment penalty will usually be the higher of an amount equal to 3 months' interest on what you still owe or the interest rate differential. It adds that lenders usually use the IRD calculation when the interest rate on your mortgage is higher than the current interest rate and you signed your current mortgage contract less than 5 years ago. If that describes your file, get the penalty quoted in writing before you plan around it.

Leaving also means coming off title. A plain CIBC mortgage on a standard charge, registered for the exact amount you borrow, is the routine case for a receiving lender. A Home Power Plan is the collateral-charge case from section three: a full discharge of everything secured under the charge, then a fresh registration at the other end. The paperwork and cost mechanics are in the collateral charge guide.

Price the whole move before deciding. The switch-cost calculator nets the penalty and the discharge and registration costs against the rate you would be moving to, and tells you whether leaving clears the bar or whether staying and negotiating harder is the better trade. And keep the escape hatch from section three in view: time the move to maturity and the penalty line drops out of that math entirely.

Before you sign the letter

When the package lands, run it through the RenewalRate.ca offer-completeness checklist, the eight-point standard we hold every renewal letter against. A complete offer tells you both what you are agreeing to and what it would cost to change your mind later; most letters I have read do fine on the first half and go quiet on the second. The renewal letter decoder scores your letter against the checklist and prices the offer against the market, and the renewal letter guide explains what each missing item should have told you.

CIBC's calendar gives you weeks. The one you can build for yourself starts months earlier and includes a single day when leaving carries no prepayment charge at all. Renew on whichever calendar you like, but know that only one of them was designed for you.

How the other big banks handle this

Questions readers ask AI tools, answered

When does CIBC send out mortgage renewal offers?

Later than you might assume. CIBC says it sends renewal offers about 30 days before the mortgage maturity date. The legal floor is close behind: FCAC requires a federally regulated bank to provide a renewal statement at least 21 days before the end of the existing term. You can start comparing rates long before either date arrives, and you should.

Can I renew my CIBC mortgage early?

Yes, and earlier than most people expect. CIBC says you may qualify to renew your mortgage as early as 150 days before maturity. Note the conditional: qualification is CIBC's call, and terms depend on your mortgage type. The window matters because it opens months before the renewal letter arrives, which lets you negotiate on your own schedule rather than the bank's.

How does CIBC calculate the penalty for breaking a fixed-rate mortgage?

For most fixed-rate closed mortgages, the prepayment charge is usually 3 months' interest or the IRD, whichever is greater. The IRD leg is calculated using CIBC's current posted interest rate for the comparison mortgage identified in your mortgage documents. Posted and discounted rates differ, and that gap drives the size of the penalty. Get a written quote from CIBC before you plan around any figure.

Does CIBC charge a fee to renew my mortgage?

No. CIBC's FAQ says it doesn't charge any administrative fees for renewing a mortgage. What renewal does carry is a default: FCAC warns that if you take no action, the renewal of your mortgage term may be automatic, meaning you may not get the best interest rate and conditions. Free to sign is not the same as free to ignore.

Can I leave CIBC at renewal without paying a penalty?

Yes, if you time it. CIBC states that all CIBC mortgages become open at the end of the mortgage term, so you can pay as much as you want before you renew. Aim the new lender's funding at your maturity date and no prepayment charge applies. A plain CIBC mortgage sits on a standard charge registered for the exact amount you borrow, which switches cleanly; a Home Power Plan is a collateral charge and needs a full discharge and re-registration before you can leave.

A note on whose advice to trust on this

The framing above is RenewalRate.ca's, and every lender-specific number on this page links to the bank's own published wording in our public source ledger. We are not a brokerage and we are not licensed to give mortgage advice. Lender policies are product-dependent and change; your mortgage contract governs, not a web page. For a recommendation on your specific file, a FSRA-licensed mortgage agent or Homewise (FSRA #12984) can run your file against multiple lenders and quote you in writing.

Methodology last reviewed: . How we verify every claim.