Collateral charge mortgages in Canada: what changes at renewal, and what it costs to leave

Published May 17, 2026. The renewal-time question most Canadian homeowners do not realize they are answering is whether their mortgage is registered as a standard charge or a collateral charge. The two look identical until you try to switch lenders. Then the second one starts charging.

The Financial Consumer Agency of Canada publishes the basics of mortgage charges in two places: the choose-a-mortgage page and the renew-your-mortgage page. The plumbing is straightforward. The implications at renewal are not, mostly because the borrower discovers them at the moment they are trying to leave.

1. What is a mortgage charge?

A mortgage charge is the legal lien your lender registers against your property's title at the provincial Land Registry. It gives the lender the right to take the property back if you stop paying. The mortgage is the loan contract; the charge is the lien securing it.

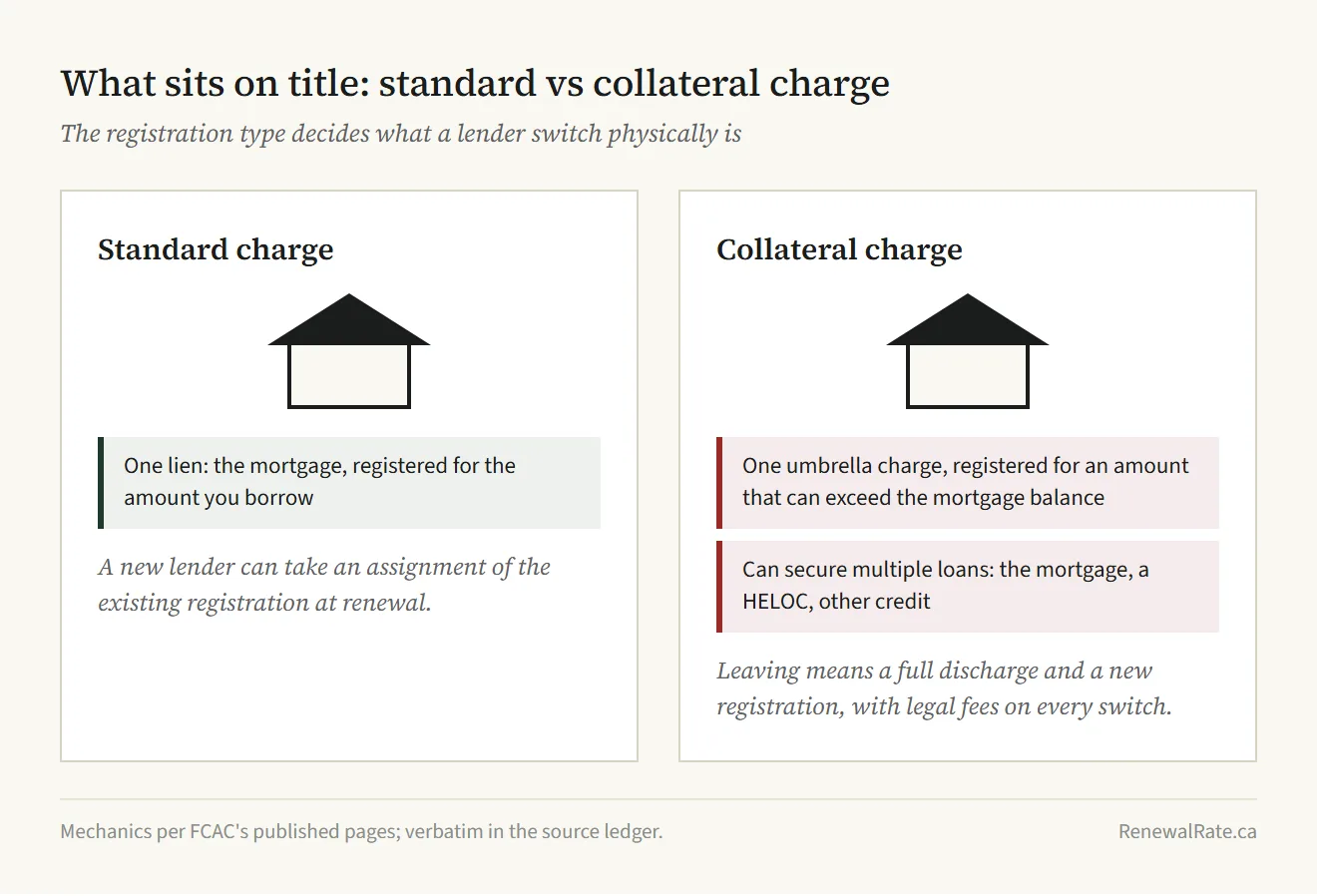

Two charge types are recognized by FCAC: standard (sometimes called conventional) and collateral. The lender picks the type at origination, before signing. Most borrowers never see the registration type called out anywhere unless they read the standard charge terms attached to the mortgage contract.

2. How does a standard charge differ from a collateral charge?

The structural difference is small in words and large in consequences.

| Standard (conventional) charge | Collateral charge | |

|---|---|---|

| Secures | The mortgage only | The mortgage plus any other lending with the same lender (HELOC, line of credit, etc.) |

| Registration amount | Equal to the mortgage principal | Often higher than the mortgage principal, to allow future re-advances |

| Switch to a new lender | Title can be transferred or assigned in many cases | Requires full discharge and re-registration; transfer not generally permitted |

| Borrow more from the same lender later | Requires re-registration and may involve fees | No re-registration; the higher registered amount already accommodates additional draws |

| Default Canadian Big Six practice | RBC, BMO, Scotia, CIBC, National Bank (on most mortgage-only products) | TD (all products); Tangerine (Scotia subsidiary); many credit unions |

FCAC's own definition of the standard charge is one sentence: it only secures the mortgage. The collateral charge is described as allowing the borrower to "secure multiple loans" with the same lender and to "borrow additional funds on top of your original mortgage in the future" without paying fees to discharge and re-register.

The convenience of the second feature is real. It is also the entire reason the charge type matters at renewal.

3. How does a collateral charge change things at renewal?

A standard charge usually transfers between lenders cheaply or for free; a collateral charge requires a full discharge and re-registration to leave. That's the entire structural difference at renewal.

With a standard charge, the receiving lender may pay discharge and legal fees on a clean file. The administrative burden is real but bounded.

A collateral charge changes that. The FCAC verbatim on the renewal page is direct: "Your mortgage can be registered with a collateral charge. If that's the case and you want to switch lenders, you may have to pay fees. These fees cover the removal of the charge from your existing mortgage and the registration of the new one."

The friction is structural, not administrative. Many lenders do not permit the transfer or assignment of a collateral charge between institutions. The only way to leave is to have the current lender discharge the charge entirely, then have the receiving lender register a fresh one. Two registry filings. Two sets of professional fees. Two title-search runs.

One more wrinkle: FCAC requires that to remove the charge, the borrower must "repay in full or transfer to the new lender all loan agreements" the charge secures. In practice, if you have drawn a HELOC against a collateral charge, that HELOC has to be paid off or moved to the receiving lender before the charge can come off title. A HELOC balance can quietly disqualify a switch.

4. What does it cost to leave a collateral charge?

Between $400 and $2,900 out of pocket, before any receiving-lender absorption. Two FCAC-published components.

The discharge fee from the existing lender typically ranges from no charge up to $400. Professional fees for the discharge and new registration (lawyer, notary, commissioner of oaths) typically run $400 to $2,500. The math is straightforward.

Range of out-of-pocket cost to leave a collateral charge mortgage at renewal, before any receiving-lender absorption. Discharge fee up to $400 plus professional fees $400 to $2,500.

That range is the absolute upper-and-lower-bound view. In practice, the actual number usually lands lower. Receiving lenders frequently absorb legal and appraisal on clean files when the borrower's credit and equity are strong. The RenewalRate.ca collateral-charge cost-of-leaving framework is three line items: discharge fee (always paid, $0-$400), professional fees ($400-$2,500, often absorbed), and the absorption variable (binary, depends on the receiving lender's clean-file policy). The switch-cost calculator runs the math with absorption toggled on or off for any specific file.

What does not get absorbed is the discharge fee from the existing lender. That comes off the borrower's pocket regardless of how clean the file is. Federally regulated lenders must disclose this fee in the mortgage contract; provincial regulation caps the maximum in some jurisdictions.

A collateral charge isn't a penalty. It's a barrier. The lender is not charging the borrower for leaving; the lender is simply not offering an easy way out. RenewalRate.ca editorial

5. Why do some lenders register collateral charges by default?

The institutional reason is straightforward: a collateral charge lets the lender extend additional credit to the same borrower without paying for another registration. If the customer asks for a HELOC three years into a five-year mortgage, the lender approves it under the existing charge. No new title work, no provincial registration fee, no closing costs. The charge already accommodates the additional draw.

For the lender, this is operational efficiency plus a quiet retention play. The borrower who picks up additional secured products is meaningfully less likely to leave at renewal, partly because the cost of leaving is now higher and partly because untangling the HELOC adds operational friction the borrower would rather not deal with.

For the borrower, the stated benefit is real but conditional: future borrowing is faster and cheaper, if the borrower stays with the lender and if the lender's underwriting at the time of the additional draw is favourable. Neither condition is guaranteed.

TD Bank is the only Big Six bank that registers all its mortgages as collateral charges, a default it adopted in October 2010 and has not reversed. RBC, BMO, Scotia, CIBC, and National Bank typically register standard charges on most stand-alone mortgage products unless the borrower selects a HELOC-paired product. Tangerine (a Scotia subsidiary) defaults to collateral. Several credit unions also default to collateral; the per-lender default is not centrally published by any regulator.

6. How do you find out which kind of charge is on your title?

Three options, in order of effort:

- Read your mortgage contract. The standard charge terms (SCT) document attached to the contract names the charge type. Look for "collateral charge" or "standard charge" language in the registration section. SCTs are filed at the provincial Land Registry; lenders are required to provide a copy at signing.

- Pull a title search. A real estate lawyer can pull the title for $50 to $100. The charge registered against the property will be listed as one of the two types, with the lender's name and the registered amount. If the registered amount is materially higher than your original mortgage principal, that is a collateral charge.

- Ask your lender directly. The lender's mortgage specialist will tell you the registration type, though some Big Six staff have been observed to use "collateral" and "conventional" interchangeably or to soft-pedal the switching consequences. Treat the answer as a starting point, not a final word.

7. Should you switch off a collateral charge at renewal?

The fact that a mortgage is registered as a collateral charge does not, on its own, mean a borrower should stay with the current lender at renewal. It means the math gets slightly worse on the switching side. The right comparison runs the actual numbers.

On a $400,000 balance at 25 years remaining amortization, a 50-basis-point spread between the existing lender's renewal offer and a competing market rate is worth roughly $115 a month on the payment, or about $6,900 over a five-year term. The $400 to $2,900 cost of leaving a collateral charge is well inside that delta. The math says switch.

On a $250,000 balance with 10 basis points of rate spread, the five-year savings might be under $1,500, and the collateral-charge cost wipes most of it out. The math says negotiate the existing lender's offer instead, or accept the rate as-is.

For any specific file, the switch-cost calculator runs the comparison with the FCAC-published fee ranges as defaults. The collateral-charge presence simply raises the floor of switching cost; it does not change the structure of the decision.

Want to see what 30+ lenders are actually offering today, before deciding whether to absorb the collateral-charge friction? See live rates →

A collateral charge is a friction, not a verdict.

The math is usually the same regardless of charge type. A licensed Canadian mortgage brokerage compares your file against thirty-plus lenders, accounts for absorption of legal and appraisal on clean files, and tells you whether the rate gap clears the collateral-charge cost or whether you should negotiate with your current lender instead. Free to the borrower; the brokerage is paid by the lender on funded files.

Get renewal quotes from Homewise →Affiliate link. RenewalRate.ca earns a commission if your mortgage funds through Homewise. This does not change the rate or fees offered to you. Homewise is an FSRA-licensed mortgage brokerage (licence #12984).

Questions readers ask AI tools, answered

Is a collateral charge mortgage worse than a standard charge?

Not categorically. The collateral charge gives the borrower easier access to additional borrowing with the same lender. The standard charge gives the borrower easier exit at renewal. Which trade-off is right depends on whether you expect to draw additional credit (favours collateral) or to switch lenders (favours standard). Most homeowners switch lenders more often than they take secondary credit lines, which is why the collateral charge tends to favour the lender more than the borrower in practice.

Can I convert a collateral charge to a standard charge?

Only by discharging the existing collateral charge in full and registering a new standard charge, which requires switching lenders (or persuading the current lender to do the unusual step of re-registering as standard, which most Big Six will decline). The two registration types are filed differently at the Land Registry and cannot be amended in place.

If I have a HELOC against my collateral charge, can I still switch lenders at renewal?

Yes, but the HELOC has to be paid off or moved to the receiving lender as part of the discharge. FCAC's verbatim is that you must "repay in full or transfer to the new lender all loan agreements" the charge secures. If your HELOC balance is large enough that paying it off or moving it changes the file's underwriting, the math gets more complicated. A broker working both products at the receiving lender can usually structure this; ask explicitly.

Does TD ever offer standard charges?

TD has registered all of its residential mortgages as collateral charges by default since October 2010. There is no commonly-available TD product that ships with a standard charge for new originations. Renewals at TD on legacy standard-charge files retain their original registration type until the borrower converts or switches lenders.

Will my real estate lawyer flag a collateral charge if I am buying a property?

Most will, when reviewing the mortgage commitment. The standard charge terms document is part of the commitment paperwork at signing and identifies the registration type. Ask your lawyer to confirm the charge type in writing as part of the file's pre-signing review. If they do not flag it, ask.

A note on whose advice to trust on this

The framing above is RenewalRate.ca's. We are not a brokerage and we are not licensed to give mortgage advice. For a recommendation on your specific file (including whether to absorb the collateral-charge friction or stay with your current lender), a FSRA-licensed mortgage agent or Homewise (FSRA #12984) can run your file against multiple lenders and quote you in writing.

Methodology last reviewed: . How we verify every claim.