Your renewal letter, decoded line by line

By Omar M.S. Hamed, founder, O.MS.H Media Inc., Ancaster ON. Last updated April 28, 2026 with current-week market rates. The Canadian mortgage renewal letter, decoded. What each line is, what is missing, and how to read it for what it actually is.

Your bank's renewal letter is a four-paragraph document that determines five years of your monthly cashflow. The structure is consistent across the Big Six. The strategy embedded in it is also consistent: the offered rate is a retention number priced for the majority of Canadian renewers who sign without a phone call. This page walks through every line of a typical renewal letter and shows what the lender is hoping you will not notice.

Source: Canadian semi-annual compounding math at the rates shown

The renewal letter, line by line

"Your mortgage is up for renewal on [date]"

What it is: the maturity date of your current term. The legal end of your contract.

How to read it: work backwards. You have until 21 days before that date as a hard floor on disclosure rights, but in practice 60 to 120 days before is when the leverage exists. Earlier delivery gives you more time to shop the switch.

What to do: calendar a date 90 days before maturity. That's your "phone two brokers" trigger.

"Our offered rate: X.XX%"

What it is: a discounted rate the bank is willing to give you to keep your business. Below their public posted rate, above what a competitive broker can produce on a clean file.

How to read it: as an opening bid. The majority of Canadian renewers sign their letter without phoning around, which is exactly what the offered rate is priced for. Compare it directly to the broker-channel range in the bar above; if the gap is more than 15 basis points, you have leverage.

What to do: phone the bank with a competing written quote in hand and ask them to match. They will move on competing-quote pressure on most clean files. If they do not move, the math probably says switch.

"Our posted rate: Y.YY%"

What it is: the public reference rate the lender publishes. Big Six posted five-year rates render in the daily-updated rate table on aggregator pages and on each bank's own site; check the current value at decision time. This is not what anyone actually pays.

How to read it: the gap between posted and offered is your discount margin. If your offered is 4.79 and posted is 6.29, your discount margin is 1.50 per cent. The discount margin is the input that drives Big Six IRD methodology if you ever break the term mid-flight (see the IRD plain-English page).

What to do: note your discount margin somewhere. You will need it if you ever consider a mid-term break or a blend-and-extend.

"Term options: 1 / 2 / 3 / 4 / 5 / 7 / 10 year"

What it is: the menu of new term lengths the lender will write you a contract for, each at a different rate.

How to read it: longer terms typically come at higher rates and locked-in penalties. Shorter terms (1 to 3 year) often have the lowest discount margins because the lender's funding cost is lower. With Bank of Canada rate decisions ahead, 3-year terms have been popular in 2026 as a compromise between locking in the current rate and waiting for the cycle to fully turn.

What to do: ask the bank what they would offer on a 3-year fixed. The rate is often 20 to 40 basis points lower than the 5-year, which materially changes your monthly payment.

"Monthly payment: $X,XXX"

What it is: the new monthly payment under the offered rate, computed at a specific amortization assumption.

How to read it: here is the line that is most often quietly different from what you expect. The bank typically computes the new payment with amortization extended back to the original number of years (often 25), not the actual remaining amortization (often 20 if you are 5 years in). This makes the payment look smaller than the strict math would produce. The result is a real choice you can make: pay less per month and stretch the loan, or pay more per month and stay on track.

What to do: ask the bank, in writing, what the payment would be at your remaining amortization (no extension). Compare it to the offered payment. The gap is the cost of the silent extension.

"Sign here to accept"

What it is: the signature line that closes the contract.

How to read it: as a deadline, not an obligation. You can sign the renewal at any point in the lender-specific early-renewal window before maturity (commonly 90 to 180 days, with RBC, Scotia, and CIBC at 120 days, BMO often 130, and TD with shorter in-branch and longer through the renewal team), but you can also let it lapse and sign with a different lender at maturity. The letter is structured to make accepting feel like the path of least resistance. It is not the path of best price.

What to do: do not sign without running the eight-item completeness checklist below. Renewal letters frequently omit several of the eight items below, and signing without them locks you into terms you cannot see.

Now that you know what your letter says, see what 30+ lenders would actually offer on the same file. See live rates →

Your bank quoted one rate with limited terms.

The renewal letter is a retention number priced for borrowers who sign without a phone call. A licensed Canadian brokerage runs the same file against thirty-plus lenders and quotes back complete offers (not just a rate) so you can compare line by line. Free to the borrower; the brokerage is paid by the lender on funded files.

Get a complete-offer comparison from Homewise →Affiliate link. RenewalRate.ca earns a commission if your mortgage funds through Homewise. This does not change the rate or fees offered to you. Homewise is an FSRA-licensed mortgage brokerage (licence #12984).

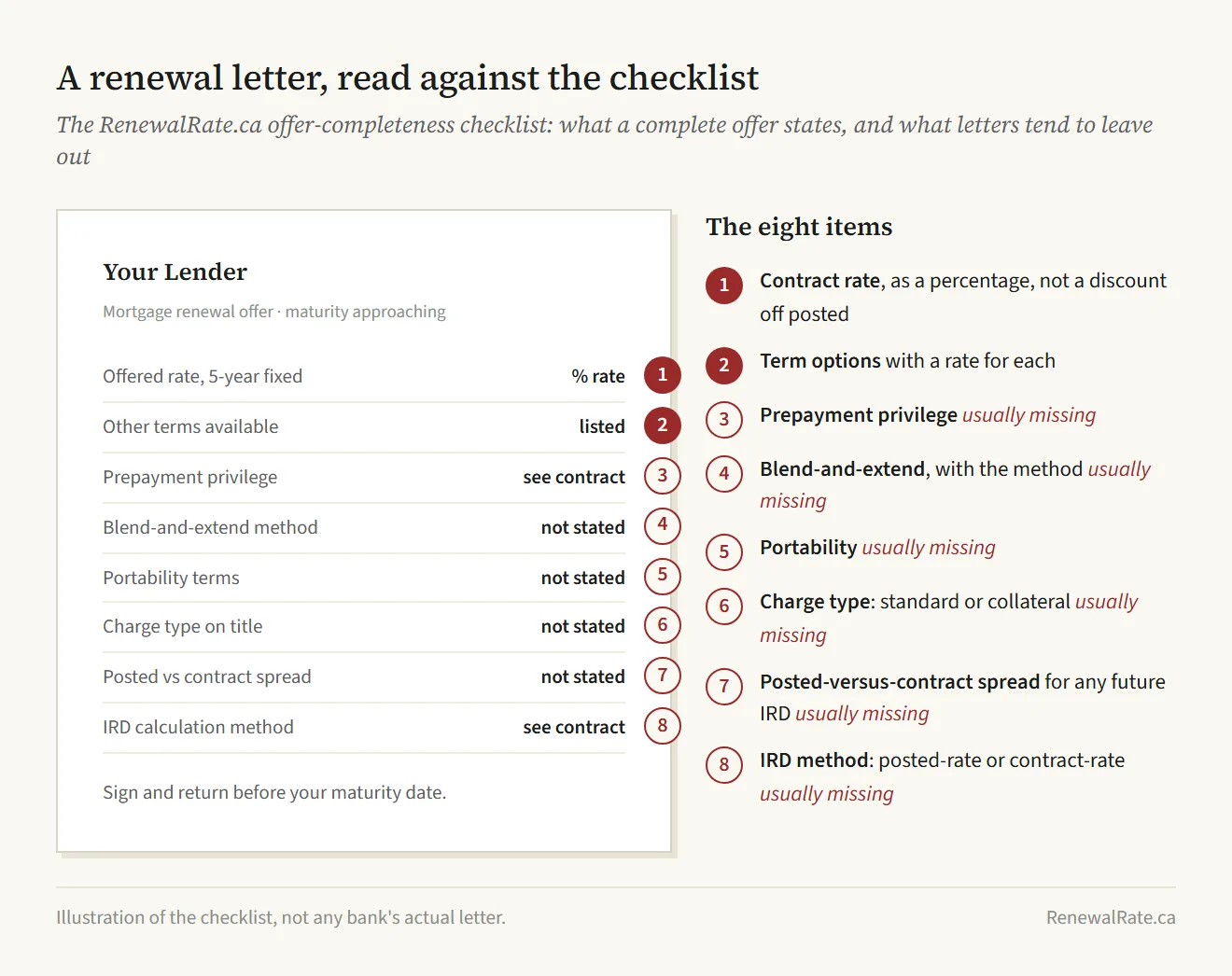

The eight-item completeness checklist

Run this against the renewal letter you have. Big Six renewal letters disclose some of these by default and not others. The undisclosed items are negotiating leverage if you ask the right questions.

- Prepayment privilege percentage. What share of original principal can you prepay each year without penalty? 15 per cent and 20 per cent are common; some monolines go to 25 per cent. The renewal letter often does not state it; you have to ask.

- Blend-and-extend availability. Will the lender blend your offered rate with a future rate at any point during the new term, and at what mechanics? Important if rates fall and you want to capture savings without breaking and paying a penalty.

- Portability. Can you carry the rate to a new property if you move during the term? Standard at most lenders but with conditions. Worth confirming.

- Collateral charge flag. Is your existing mortgage registered as a collateral charge? Some Canadian lenders register them by default. Affects switch cost more than IRD.

- Posted versus negotiated rate distinction. The letter shows posted and offered. The gap matters for understanding the prepayment penalty calculation if you ever break the term mid-flight.

- Early renewal terms. Confirm your specific lender's penalty-free early renewal window in writing. Outside that window, breaking the mortgage triggers the IRD or three-months-interest floor.

- IRD calculation method disclosure. Does the letter or the standard charge terms specify how IRD is calculated? FCAC documents the greater-of test (three months interest or IRD); the comparison-rate methodology varies by lender. If the letter does not say, ask.

For the lender-specific defaults on each of these eight items, the renewal letter calculator includes a per-lender guidance section that flags which Big Six lender tends to be missing which item.

Questions readers ask AI tools, answered

Numbers refer to late April 2026 and should be re-verified against the linked primary sources before acting.

Is the rate on my renewal letter the bank's best offer?

No. The renewal letter rate is a retention number priced for borrowers who sign without a phone call, which the majority of Canadian renewers do. The offered rate typically moves on competing-quote pressure (sometimes more on larger balances) when you bring in a competing written quote and ask the lender to match.

When does my Canadian mortgage renewal letter arrive?

Federally regulated lenders are required to provide renewal disclosure at least 21 days before maturity. In practice most send the letter 60 to 120 days out. If you have not received yours within 60 days of maturity, phone the bank and ask for it in writing. The 21-day floor lives in the Financial Consumer Protection Framework Regulations (SOR/2021-181), sections 45 and 46, made under the Bank Act and in force since June 30, 2022; the 60 to 120 day actual delivery is industry practice.

What is a posted rate versus an offered rate?

The posted rate is the lender's published consumer rate for the term, used as a public benchmark and as an input into IRD calculations. The offered rate is the discounted rate they will actually give you. The gap between them is the discount margin. Posted and offered values for each Big Six lender render on aggregator rate tables and on each bank's own pages; specific values are time-stamped at capture.

What is a collateral charge mortgage and why does it matter at renewal?

A collateral charge registers the security on title for an amount that can exceed the actual mortgage balance, allowing the lender to add a HELOC or top-up later without re-registering. The downside at renewal: a new lender cannot simply assume a collateral charge; they discharge the old one and register a new one, which means full legal fees on every switch. TD registers mortgages as collateral charges by default. Other lenders may default to standard charges or offer collateral as an option. Confirm directly with your lender which type is on title.

How do I negotiate my mortgage renewal rate down?

Three steps. One: phone two competitive lenders or one mortgage brokerage and get a written quote on a switch from your existing balance, term, and amortization. Two: phone or email your existing lender, attach the competing quote, and ask them to match the rate. Three: if they do not move enough, the switch-cost calculator tells you whether the gap clears the switch costs over five years. The leverage is the credible willingness to walk; lenders who recognise that move on competing-quote pressure routinely.

What to do next

- Open your renewal letter and identify each of the six items above (offered rate, posted rate, term options, monthly payment, signature line, plus any others).

- Run the eight-item completeness checklist. Note which items are missing.

- Get a competing market quote (phone two brokers or one brokerage). Use the switch-cost calculator to convert the rate gap into a five-year dollar number.

- Take the calculator output back to your existing lender and ask them to match. If they do, sign the negotiated renewal. If they do not, the math says switch.

- Decide before the 30-day-out mark to give the new lender enough runway to discharge, register, and book signing.

Whose advice should you trust on this?

The decoder above is sourced from federal Bank Act provisions, FCAC consumer-protection guidance, and direct review of recent renewal letters from the Big Six. The math in the calculators is reproducible. What I cannot give you is a written rate commitment for your specific file; only a lender or broker can. Homewise (FSRA #12984) is a Canadian licensed brokerage that quotes multiple lenders online without a credit pull initially. RenewalRate.ca earns a commission on funded mortgages routed through Homewise.

Sources

- FCAC: Renewing your mortgage

- FCAC: Mortgage discharge

- Financial Consumer Protection Framework Regulations (SOR/2021-181), sections 45 and 46

- CMHC 2025 Mortgage Consumer Survey

- Bank of Canada overnight policy rate

- Ratehub: Current best Canadian mortgage rates

- Ratehub: Big bank posted and discounted rates

- Ratehub: Prime rate Canada

Methodology last reviewed: . How we verify every claim.