Canadian mortgage renewal: a complete 2026 guide

Published April 23, 2026. Written for homeowners facing a renewal in the next 24 months.

If your five-year fixed was signed sometime between 2021 and 2023, you are now walking into the sharpest rate transition Canadian homeowners have faced since the early 1990s. The gap between what you signed at and what the market will offer you in 2026 is, for most files, between 150 and 250 basis points. That is the entire story. The rest of this guide is the mechanics: what renewal means in its narrow legal sense, what actually happens in the ninety days before you sign, and where the math lines up for most households.

1. What is mortgage renewal in Canada?

A renewal is the moment your mortgage term ends and the lender asks you to sign a fresh contract on the same balance you still owe. No house is being bought. No new money is being borrowed. The principal is the same principal, and the deal is only about what rate and what term get stamped on it next.

Two things get mixed up with renewal all the time. One is refinancing, which is a separate product. Refinancing means you are breaking or restructuring the mortgage, usually to pull equity out of the home, stretch the amortization, or roll other debt into it. That involves an appraisal, a full underwriting run, and if it happens before maturity, a penalty that can bite hard.

The other is a new purchase. Unless you switch lenders, you do not face the federal stress test at renewal the way a first-time buyer does. Staying put means the bank already has your file and is not running it through the wringer again. Switching is its own set of rules, handled later in this piece.

Strip it down: renewal is the lender asking you to sign again. Everything else in this article is the question of whether you sign what they put in front of you, or whether you sign somewhere else.

2. Why is the 2026-2028 renewal window specifically painful?

The Bank of Canada's Financial Stability Report 2025 found that roughly 60 per cent of outstanding Canadian mortgages renew across 2025 and 2026 combined, and that about 60 per cent of those renewing borrowers will see a higher payment than they were carrying before. The product of the two figures, around 36 per cent of all outstanding mortgages facing a payment increase at this renewal cycle, is the share that drives the macro-stability framing in the FSR. Most of these contracts were signed when the overnight rate sat at 0.25 per cent, back when a lender would quote a five-year fixed under 2 per cent without blinking. The rates they are renewing into have cooled off the 2023 peak but remain far above where these borrowers started.

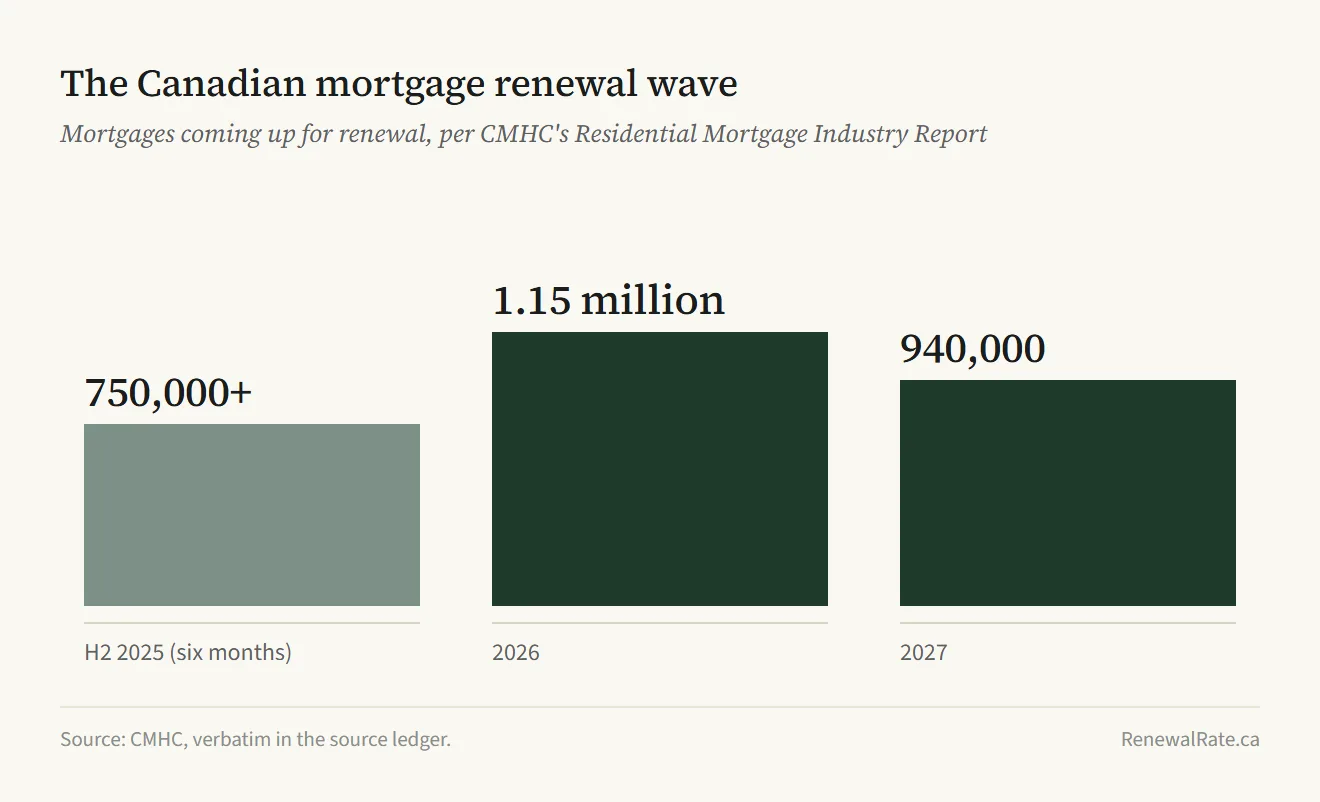

CMHC has put harder numbers on the timing. Its Residential Mortgage Industry Report for Fall 2025 projects roughly 1.15 million renewals in calendar 2026, followed by another 940,000 in 2027. Two million households in the same rate-shock queue, staggered across twenty-four months like a long freight train crossing a single bridge.

Ratehub.ca ran the representative case in April 2026. A borrower who took a typical five-year fixed at pandemic-era rates will see the monthly payment jump by about $622, or 24 per cent, at renewal. That is the median. Your own number depends on the balance you are carrying, how much amortization is left, and what you originally locked in at.

There is a narrow piece of good news in the Bank of Canada data: the average payment increase has come in below what the market was pricing during the recent rate-cycle peak. That is a real relief at the aggregate level. It does not translate into a small number at the kitchen table. A $622 monthly increase on a single household budget is the cost of a car payment, arriving every month for five years, without anyone handing you a car.

Average monthly payment increase for borrowers renewing a five-year fixed in April 2026, on a typical balance.

Source: CMHC, Residential Mortgage Industry Report Fall 2025

If you want to see what your specific payment shock looks like, the payment-shock calculator is the fastest way. Put in your current balance, your old rate, and today's offered rate, and it will show you the dollar difference.

3. What happens in the 120 days before renewal?

Federally regulated lenders must notify you of your renewal terms at least 21 days before maturity; renewal letters typically arrive 90 to 120 days out. That three-to-four-month window is where almost all the leverage sits, and where most of the money gets saved or lost.

At 120 days: request a rate hold

Around the 120-day mark, request a rate hold from your current lender and from any competing lender or broker. A rate hold locks a rate at today's pricing; if rates fall between now and signing, any reputable lender drops you to the lower rate. The hold does not commit you to anything. It keeps the door open at a known price.

At 90 days: read the renewal letter as an opening offer

Roughly 90 days out, the renewal letter shows up. Some lenders send it earlier, some closer to 60. The letter lists a posted rate and a so-called special rate that sits underneath the posted rate and above what a broker can pull from a competing monoline. Read it as an opening offer. That is what it is.

At 60 days: the decision becomes real

By 60 days out, the useful inputs should be in front of you: a comparison quote or two, your exact mortgage balance, the amortization left on the clock, and any lump-sum prepayment already made in the current term. If those four numbers are not on a single sheet of paper yet, this is the week to put them there.

At 30 days: execution

The final 30 days are execution. A switch has the new lender ordering the discharge, pulling title, and booking the signing with a real estate lawyer or notary. A stay has a renewal agreement coming back for signature. Either way, the interesting decisions were made before this window opened.

Should you renew early?

Usually no, unless rates are falling fast. Most lenders allow early renewal in the final 120 days without penalty. Earlier than that, you are breaking the mortgage and triggering a prepayment penalty: the larger of three months' interest on the balance or the lender's interest rate differential (IRD) calculation. In falling-rate cycles, IRD at the Big Six can run into five figures. In 2026, with most renewing borrowers holding sub-2 per cent contracts and current rates in the mid-4s, the three-months-interest floor governs and penalties land in the low four figures rather than five. See our IRD plain-English explainer for the math.

4. What are your three real options at renewal?

Stay with your existing lender, switch lenders, or refinance. Three options, and only three. Everything else marketed to renewing homeowners is one of these three with a different name.

Option A: Should you stay with your existing lender?

Stay only if your file has changed enough that requalifying would be a problem, or if the gap between your lender and the best competing quote is inside five basis points after switching costs. The argument for staying is friction, not rate: no discharge, no lawyer, no appraiser, no fresh underwriter. The existing lender already owns the risk and will usually roll you over without re-opening the credit file. The argument against staying is pricing: the rate in the renewal letter is a retention offer, priced on the assumption you will sign without a phone call. Bring a written competing quote, the number usually moves. Bring nothing, it stays where it is.

Option B: Should you switch lenders via a broker?

For borrowers with clean files, switching is where most of the money is saved. Switching at renewal does not trigger the interest rate differential penalty, because the old term is ending on its own schedule. The new lender re-underwrites the file, usually orders an appraisal, and on a qualifying balance frequently absorbs the discharge fee and legal bill.

One regulatory development matters. Effective November 21, 2024, OSFI exempted uninsured straight switches from the prescribed Minimum Qualifying Rate stress test. Standard B-20 underwriting still applies (income, credit, capacity), but the contract-rate-plus-two-per-cent or 5.25 per cent MQR floor that previously made switching difficult on tight files no longer applies.

CMHC's Fall 2025 Residential Mortgage Industry Report shows uninsured-lender switches climbing roughly 67 per cent year over year to about $19 billion. The curve is going in one direction, and brokers and monolines like First National, MCAP, and Equitable Bank are a big part of the reason.

Brokers are compensated by the lender on funded files, not by the borrower. Zero out-of-pocket cost to the client. What a broker sells is access to roughly thirty lenders instead of one, plus the paperwork-wrangling function most people badly undervalue until they try it themselves. On a clean file, a competent broker frequently beats the in-branch retention rate without the client having to argue. Homewise is an FSRA-licensed Canadian brokerage that quotes multiple lenders online.

Option C: Should you refinance at renewal?

Refinance only if you need to pull cash from home equity or materially change your amortization. If you are only after a better rate, that is a switch, not a refinance, and the mechanics are different. Refinancing at renewal avoids the interest rate differential penalty (the term is ending anyway), but you still face a full requalification including the stress test at the qualifying rate, a new appraisal, and legal fees. If your debt-to-income has crept up or your equity position has softened, a refinance can get declined where a straight switch would have gone through. If the only thing you are trying to change is your rate, do not refinance. Switch.

5. What is a 10-basis-point rate difference actually worth?

Pick a realistic case. A $500,000 balance, 25 years of amortization left, and a 10-basis-point spread between two offers. That single tenth of a percentage point is worth about $28 a month on the payment, or $1,680 across a five-year term. On its own, not a sum that changes anyone's life. It is, however, usually bigger than the switching costs in a qualifying file where the new lender absorbs nothing.

The story gets more interesting as the spread widens. A 30-basis-point gap, which is roughly the typical distance between a retail bank's first offer and a broker's best rate for a clean Toronto or Calgary file, puts about $85 a month on the line. Over the term, that is $5,100. A 50-basis-point spread, not uncommon on the same $500,000 file when the bank's first offer is benchmarked against the broker market, runs about $142 a month and $8,500 over the five years.

The payment-shock calculator on this site will run the numbers for any specific file. The broader point is worth stating bluntly: the gap between what a bank puts on the renewal letter and what is actually available in the Canadian market is almost always wider than the cost of walking to a different lender. Borrowers who stay tend to be optimizing against the weight of paperwork, not against dollars. The paperwork is finite. The basis points are not.

Borrowers who stay at renewal tend to be optimizing against the weight of paperwork, not against dollars. The paperwork is finite. The basis points are not. RenewalRate.ca editorial

See what 30+ lenders are actually offering on a 5-year fixed today. See live rates →

Ten basis points on a $400K renewal is around $1,300 over five years.

The renewal letter is a retention rate priced for borrowers who do not phone around. A licensed brokerage runs the same file against thirty-plus lenders and quotes back the actual market rate, not the loyalty rate. Free to the borrower; the brokerage is paid by the lender on funded files. The hold runs ninety to one-hundred-twenty days and commits you to nothing.

See what thirty-plus lenders would offer on your renewal →Affiliate link. RenewalRate.ca earns a commission if your mortgage funds through Homewise. This does not change the rate or fees offered to you. Homewise is an FSRA-licensed mortgage brokerage (licence #12984).

6. What does it actually cost to switch lenders at renewal?

The cost of switching a mortgage at renewal comes from a discharge fee from the old lender (FCAC publishes that this typically runs from no charge up to $400 where unregulated) plus professional fees ($400 to $2,500 per FCAC) for legal or title-transfer work on the new side. Some files require an appraisal as well. The full envelope before any lender absorption is the sum of FCAC's component ranges; see FCAC: Mortgage discharge.

What a lot of renewing homeowners do not realise is that absorption is common. Competitive lenders regularly cover the legal fees and sometimes the discharge on clean-file switches, especially when the balance sits above $300,000. A broker will know which of their lender partners is running a cash-back or legal-absorption program on the week you file. It is not a universal rule, and it is not a promise. It is common enough that the question deserves to be asked before any cost estimate gets baked in.

Even in the unusual case where every fee lands on the borrower, the arithmetic usually still favours moving. A 20-basis-point improvement on a $500,000 balance produces roughly $3,400 in savings over five years. Net of $1,500 in switching costs, the homeowner is $1,900 ahead, and that is treating the savings conservatively and the costs generously.

The trap is psychological rather than mathematical. A $1,500 cheque written at closing feels concrete. An $85 saving that shows up once a month for five years feels abstract. The first number is smaller than the second by a factor of four, but it is the one people guard. The fix is simple enough: pull the actual numbers out of the calculator before deciding which of them is the expensive one.

7. When should you use a broker vs go direct?

Use a broker if your file is clean and you want the best rate with the least personal effort. Go direct if your situation is unusual and you need a specific lender's underwriting flexibility.

The honest take: for a typical salaried borrower with a stable income, a good credit score, and a reasonable loan-to-value ratio, a broker is almost always the better move at renewal. They have access to more lenders, they do the paperwork, and they are paid by the lender, not you. The downside is that their lender roster skews toward the ones that pay the best broker commissions, which usually means monoline lenders rather than the big banks. That is not a problem for most borrowers. The monolines often have better rates. But it is worth knowing.

Go direct to a specific bank if you are self-employed with inconsistent income, if you are near retirement and your lender has a specific retirement product, if you hold meaningful assets at one of the big six and can negotiate a relationship-based rate, or if your file has a complication that a particular lender is known to underwrite well.

If you do not know which category you are in, start with a broker. If the broker cannot place you at a competitive rate, you will learn quickly, and you can pivot to going direct with better information than you had at the start.

8. What should you watch for in the fine print?

There are three items in the fine print that carry outsized financial weight. None of them appear in the marketing copy. All three have cost Canadian homeowners five-figure sums through pure inattention.

Collateral charges vs standard charges

A handful of Canadian lenders register the mortgage as a collateral charge rather than a standard charge. The practical difference shows up at renewal. A collateral charge lets the lender sit on a registered amount that can be higher than the actual balance outstanding, which is useful when the same bank wants to offer you a line of credit later without pulling fresh paperwork. It is less useful when you decide to leave. A new lender cannot simply assume a collateral charge. They have to discharge the old one and register a new one from scratch, which means paying legal fees on both sides of the transaction every time the mortgage moves.

Some Canadian lenders register collateral charges by default. Ask the lender directly which type of charge is on title if the answer is not obvious from the original paperwork. Having a collateral charge does not kill the case for switching. It does trim the dollar advantage by a few hundred dollars, which matters on the narrow-spread cases and barely registers on the wide ones.

IRD penalties if you break early

Anyone thinking about breaking a current mortgage early, to lock in a better rate before the term actually ends, needs to obtain the penalty quote in writing first. Nothing else. That single document tells you whether the plan is realistic.

The structural feature most pieces gloss over is cycle direction. The Interest Rate Differential calculation only produces a meaningful penalty when the comparison rate the lender uses is materially below your contract rate, which happens in falling-rate cycles. In rising-rate cycles, when you locked at a low rate and current rates are higher, the IRD differential is zero or negative and the three-months-interest floor governs.

For a $500,000 balance broken in 2026, the answer depends on which side of the cycle your contract sits. In an illustrative scenario where the contract rate is 1.79 per cent and current market is 4.29 to 4.59 per cent (per the April 29, 2026 Ratehub Big 5 capture: RBC at 4.29 per cent, CIBC and Scotiabank at 4.49 per cent, BMO at 4.51 per cent, TD at 4.59 per cent), the IRD differential is negative, the three-months-interest floor governs, and the penalty is roughly $2,200 at any lender. If you signed at 5 per cent or higher and rates have since fallen, real IRD applies, and the same $500K balance can produce a materially larger penalty under a posted-rate IRD methodology than under a contract-rate methodology. Specific dollar outputs depend on each lender's posted-rate inputs at the time of breakage. For the methodology breakdown, see the IRD plain-English page.

Rate-hold timelines

Rate-hold lengths are lender-specific and disclosed at quote time. If your renewal is further out than the offered hold, you cannot lock yet, but you can ask the broker or lender to set a calendar reminder at the earliest lockable date. Do not assume the quote you got six months ago still applies. It does not.

9. What if your renewal isn't standard?

This section is brief because each of these cases deserves its own article. If one of these applies to you, the general guidance here is a starting point, not a plan.

Denied at renewal. This is more common than most homeowners expect, particularly since OSFI's B-20 guideline tightening cycles. In most cases the refusal is not a reading of the borrower's creditworthiness but a signal that the lender's internal risk appetite has shifted on the kind of file they used to accept. A broker can typically place a denied A-lender file with a B-lender or a monoline at a higher rate; specific spreads depend on the file. The practical move is to start that conversation at least 60 days ahead of maturity, because B-side underwriting runs slower than A-side underwriting.

Credit events since last renewal. Late payments, a consumer proposal, a collections account. A clean A-lender switch may not be available, but your existing lender will usually still renew you because they are not running a new credit pull. Stay with the existing lender, use the term to rebuild, and plan to shop at next renewal.

Retirement-age borrowers. Income from pensions, RRIFs, and investment accounts is treated differently by different lenders. Some are friendly to retirees. Some are not. This is a case where going direct to a lender with a strong retiree product, or working with a broker who specializes in it, can meaningfully change your outcome.

Self-employed or new-business income. The T1 General and Notice of Assessment are what lenders underwrite on. If your business is less than two years old or your stated income is significantly higher than your tax filings show, expect friction. Alt-A and B-lenders have products designed for this. They charge a premium, but they exist.

10. The RenewalRate.ca 30/60/120-day renewal checklist

The following is the sequence that actually drives outcomes, broken out by how far from maturity the file sits.

At 120 days out. Pull your most recent mortgage statement and confirm your balance, maturity date, current rate, amortization remaining, and whether your mortgage is a standard or collateral charge. Run the payment-shock calculator to see what today's rates would mean for your payment. Request a rate hold from a broker or from one or two competing lenders. No commitment. Free information.

At 90 days out. Your lender's renewal letter should arrive. Read the rate they are offering. Compare it to the rate holds you already have. If the gap is more than 10 basis points, start a serious conversation with a broker about switching. If your file has complications, this is the point where you want to know whether switching is realistic.

At 60 days out. Decision point. If you are staying, call your lender and negotiate. Tell them specifically what the competing offer is. Ask for a rate match or improvement. Get the new rate in writing before you agree. If you are switching, your broker should be submitting the application now. Documents required typically include: most recent mortgage statement, property tax bill, proof of home insurance, and income verification.

At 30 days out. Paperwork week. If switching, the new lender orders discharge from your old lender, legal work is scheduled, and signing happens. If staying, the renewal agreement gets signed and returned. Do not miss the deadline. If your old term expires without a signed renewal, many lenders auto-convert you to a variable or open mortgage at a posted rate, which is almost always worse than any negotiated option.

When should you actually act?

If you are renewing in 2026 or 2027 and you have not started, start now. The difference between the rate you end up with and the rate you could have had is usually decided in the first conversation, not the last one. A 15-minute quote from a broker costs you nothing and gives you a real number to negotiate with or walk away on.

Homewise is one of the faster ways to see multiple lender quotes online.

If you would rather compare on your own, the payment-shock calculator will show you what the rate difference actually means in dollars on your specific balance.

This guide does not argue for staying, switching, or refinancing. It argues for the borrower running the arithmetic before the lender's letter runs it for them. The Canadian mortgage market is one of the few consumer finance categories in which the price on the offer letter has almost no relationship to the price available in the same market the same afternoon, and the only remedy is a borrower who asks.

Frequently asked questions

When does the mortgage renewal process actually start?

Most lenders begin the renewal process 90 to 120 days before your maturity date, when they send a renewal letter. You can start gathering competing quotes even earlier, but rate holds from most lenders max out at 120 days.

How early can I renew my mortgage without a penalty?

Most lenders allow early renewal within the final 120 days of your current term with no penalty. Earlier than that and you are breaking the mortgage, which usually triggers an interest rate differential penalty on a fixed-rate product. Get the penalty quote in writing before deciding.

Is switching lenders at renewal worth it for a small rate difference?

On a $500,000 balance, a 10-basis-point rate improvement is worth about $28 per month, or $1,680 over five years. At 30 basis points, it is about $5,100. Switching costs are typically $1,000 to $2,500 and are often absorbed by the new lender on qualified files. For clean files, switching usually wins after the math.

What is the difference between a mortgage renewal and a refinance?

Renewal means signing a new contract for the remaining balance of your existing mortgage at the end of its term. Refinance means restructuring the mortgage to pull out equity, change amortization, or consolidate debt, which requires full requalification and usually a new appraisal.

Do I have to requalify when I renew?

Not if you stay with your existing lender. If you switch lenders, you will requalify with the new lender (income, credit, capacity), but as of November 21, 2024, OSFI no longer requires the prescribed Minimum Qualifying Rate stress test on uninsured straight switches at renewal where the balance, amortization, and borrowers stay the same. The new lender qualifies you at the contract rate, not the contract rate plus 2 per cent or 5.25 per cent. Refinances and switches that change amortization, balance, or borrowers still face the stress test. Source: OSFI MQR exemption announcement.

What is a mortgage renewal penalty in Canada?

There is no penalty to renew at the end of your term. A penalty only applies if you break the mortgage early, before maturity. For fixed-rate mortgages, that penalty is usually the greater of three months interest or the interest rate differential calculation, which can be thousands of dollars on a big-bank fixed-rate product.

Should I use a broker or go direct to my bank?

For a typical salaried borrower with a clean file, a broker usually delivers a better rate with less effort, and the broker is paid by the lender rather than by you. Go direct to a specific bank if your situation is unusual, such as self-employed income, near-retirement with specific pension-income considerations, or a long-standing relationship with negotiating leverage at one of the big six.

About this article

Published: April 23, 2026

Last updated: April 28, 2026 (specialist fact-check pass: corrected IRD cycle-direction framing in Section 8 and Section 3, added OSFI November 2024 MQR exemption to Option B and FAQ, named Big Six explicitly)

Methodology note: All rate arithmetic in this article uses standard Canadian amortization formulas (blended monthly payments, semi-annual compounding for fixed-rate mortgages) at the balances cited. Where ranges are given for switching costs, they reflect the range observed across major Canadian lenders in early 2026 and are not a quote for any specific file. The qualitative framing on renewal risk follows the Bank of Canada's Financial Stability Report 2025. Readers should confirm their specific numbers with their lender or broker before acting.

Sources:

- Bank of Canada, Financial Stability Report 2025 (published May 2025). Qualitative framing on the share of mortgages facing increases at renewal and on the average expected increase relative to 2023 market expectations.

- Bank of Canada, Staff Analytical Note 2025-21: How will mortgage payments change at renewal? (July 2025). Average payment-increase magnitudes for five-year fixed renewals.

- Canada Mortgage and Housing Corporation, Residential Mortgage Industry Report, Fall 2025. Projection of 1.15 million renewals in 2026 and 940,000 in 2027. Uninsured-lender switching activity reported at roughly $19 billion, up about 67 per cent year over year.

- Canada Mortgage and Housing Corporation, 2025 Mortgage Consumer Survey. Renewer behaviour, amortization choices, and credit-facility usage.

- Ratehub.ca, renewal payment-increase calculation, April 2026. Reported a $622 monthly increase (approximately 24%) for a typical five-year fixed renewal.

Affiliate disclosure: renewalrate.ca earns commissions from FSRA-licensed brokerage partners including Homewise when readers sign through partner links. These commissions do not affect the rates quoted to readers. Editorial content is not reviewed by partners before publication. Full details on our Disclosure page.

Methodology last reviewed: . How we verify every claim.