For files locked at sub-2 per cent rates breaking in a 4 to 5 per cent market, your prepayment penalty is the three-months-interest floor. The IRD calculation returns zero in this rate cycle. On $400,000 at 1.79 per cent, that's $1,790. The calculator confirms it for your specific balance, and the lender-by-lender section below explains the case where IRD does apply.

If you have a fixed-rate Canadian mortgage and you are considering breaking it before maturity, the Interest Rate Differential is the number you need to understand before anything else. Two things to know up front, both verified against lender standard charge terms and against the Financial Consumer Agency of Canada's published guidance.

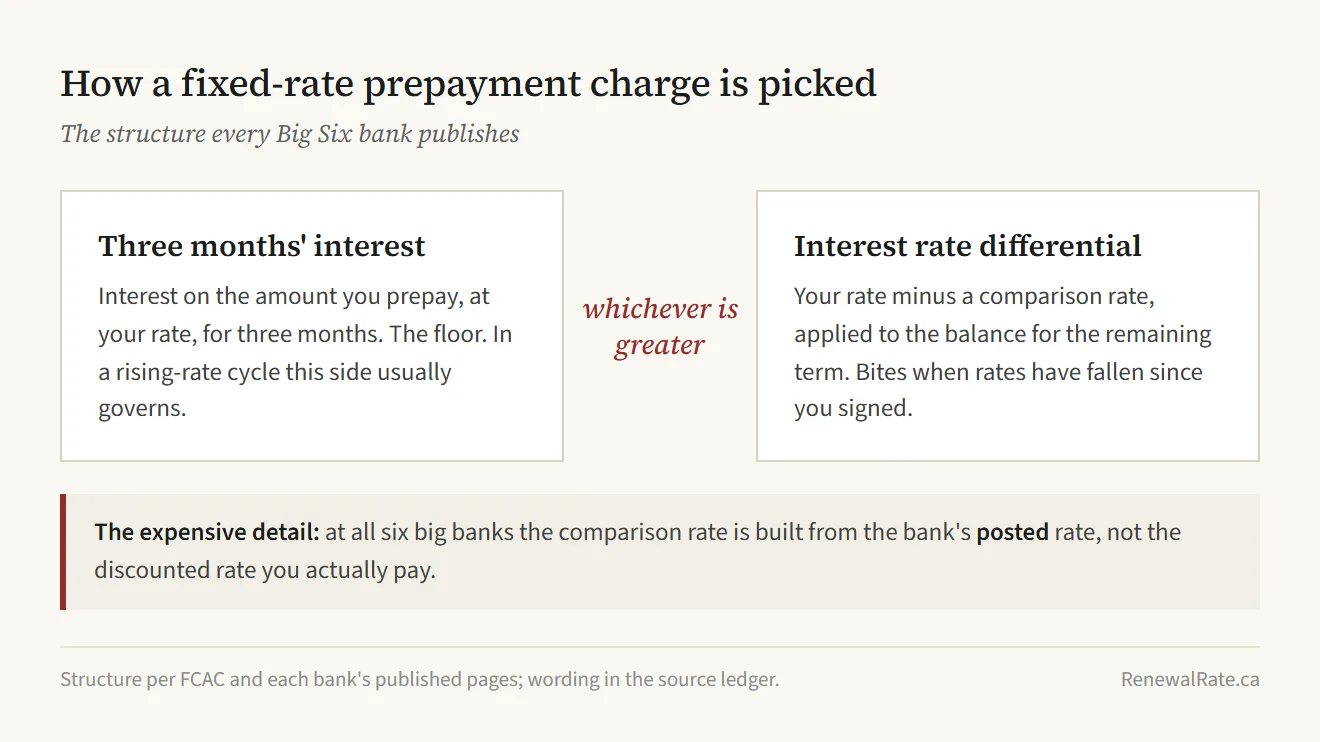

One: every fixed-rate Canadian mortgage has two penalty calculations running in parallel. The actual penalty is the larger of them. The first is the three-months-interest floor. The second is the IRD calculation. In a rising-rate cycle, the two collapse to the same number because IRD returns zero.

Two: when IRD does apply (a falling-rate cycle, not the current one), the way it's computed varies materially by lender. The Big Six use posted-rate methodology with a discount-margin reduction. Most credit unions and monoline lenders use contract-rate methodology. The same file can produce a $9,000 penalty at one and a $4,000 penalty at the other.

Why does the rate-cycle direction matter for IRD?

IRD only produces a meaningful penalty when the comparison rate the lender uses is materially below your contract rate. That condition is met in falling-rate cycles, when you locked at a high rate and rates have since fallen. The lender claws back the spread between what you committed to pay and what they could re-lend the money at today.

In rising-rate cycles, the condition is not met. You locked at a low rate, rates have since risen, and the differential between your contract rate and the lender's current comparison rate is zero or negative. The IRD calculation returns zero. The three-months-interest floor governs.

For Canadian borrowers maturing in 2026 with contract rates from 2020 to 2022 (typically 1.5 to 2.5 per cent) facing current market rates of 4 to 5 per cent, the cycle direction is unambiguously rising. The penalty defaults to the floor for almost every file in this cohort, regardless of which lender you are with. Lender-by-lender method matters less than the cycle direction.

This is the single most important thing to know before reading any further. If your contract rate is below current market, the floor is your answer. The rest of the page is about the case where it is not, plus the worked floor calculation for the case where it is.

What is the three-months-interest floor?

The floor is the minimum penalty for a fixed-rate Canadian mortgage. Multiply your current balance by your contract rate, divide by 12, multiply by 3.

On a $400,000 balance at a 1.79 per cent contract rate, that arithmetic is: $400,000 × 0.0179 ÷ 12 × 3 = $1,790. That is the floor. In a rising-rate cycle, that is also the answer.

The floor exists because lenders need an administrative fee threshold for breaking a contract that does not depend on rate movements. Variable-rate mortgages typically use only the three-months-interest method (no IRD), so for variable holders the floor is always the answer regardless of cycle direction.

How do the Big Six banks compute IRD?

RBC, TD, Scotiabank, BMO, CIBC, and National Bank publish posted-rate IRD methodologies on their consumer prepayment-charge pages. The structural form of the calculation has three inputs:

First, the lender's posted rate at the time you signed your current term. This is not what you actually paid; it is the lender's published five-year fixed rate on the day your mortgage started. Posted rates are materially above what well-qualified borrowers actually receive. Big Six posted five-year rates and discounted offers render in the daily-updated rate tables on aggregator pages and on each bank's own site. Specific values are time-stamped at capture; check current values at decision time.

Second, the discount margin you received at origination. If your posted rate at signing was 4.79 per cent and your contract rate was 1.79 per cent, your discount margin was 3.00 per cent. The lender takes the discount margin as a fixed reduction on the comparison rate.

Third, the lender's current posted rate for a term equal to your remaining months. If you have 18 months left, the lender uses their current posted rate for the closest available term (often the two-year posted rate, or a calculated rate via interpolation). Apply your discount margin reduction to this comparison.

The IRD differential is then your contract rate minus the discounted comparison rate. If positive, multiply by remaining balance and divide by 12, multiply by remaining months. If zero or negative, the floor governs.

The discount-margin reduction is the part most readers find counterintuitive. The lender uses your old discount margin against their new posted rate, which can produce a comparison rate that does not match any rate available in the market. In falling-rate cycles, this widens the differential and increases the penalty. In rising-rate cycles, it does not help the borrower; the IRD is already zero before this step matters.

Lender prepayment-charge methodology is documented on each lender's consumer-facing prepayment-charge or FAQ page, and in the standard mortgage charge terms filed in provincial land registries. Methodology details vary by lender; the mechanic is broadly similar across the Big Six.

How do credit unions and monoline lenders compute IRD?

Most credit unions and MCAP use contract-rate IRD. Other monoline lenders typically follow the same convention. Two inputs.

First, your actual contract rate (not posted rate, not posted-minus-discount).

Second, the lender's current discounted rate for a term equal to your remaining months.

The IRD differential is the contract rate minus the current discounted rate. Apply to balance over remaining months as above.

Because the comparison rate is the current discounted rate (not the posted rate minus your old discount margin), the contract-rate computation tends to differ from the Big Six method in falling-rate cycles. The size of the gap depends on the original discount margin and the spread between posted and discounted at the time of break.

In rising-rate cycles, the contract-rate method also returns zero or negative, so the floor governs at credit unions and monolines just as it does at the Big Six.

The penalty math only matters if a competing offer beats it. See what 30+ lenders are offering today. See live rates →

The penalty math only matters if a competing offer exists.

You cannot price an IRD penalty in isolation. The decision is the differential between staying and switching, net of penalty plus switch costs. A licensed brokerage runs your existing rate against thirty-plus discounted offers and produces the net dollar number that walks the decision. Free to the borrower; paid by the lender on funded files.

Get a switch quote from Homewise →Affiliate link. RenewalRate.ca earns a commission if your mortgage funds through Homewise. This does not change the rate or fees offered to you. Homewise is an FSRA-licensed mortgage brokerage (licence #12984).

What does IRD actually look like under 2026 conditions?

Two representative files. Every number is reproducible by entering the inputs into the calculator above.

The 2026 cohort: $400K, 1.79 per cent, 18 months remaining (Big Six)

Floor: $400,000 × 0.0179 ÷ 12 × 3 = $1,790. IRD: posted-rate method against the Big Six's current 2-year posted rate (refer to the Bank of Canada weekly chartered-bank posted-rate series for the current value), less your original discount margin margin, gives a comparison of 3.09 per cent. Your 1.79 per cent contract rate is below 3.09 per cent, so the differential is negative 1.30 per cent. IRD returns zero. Actual penalty: $1,790. Same arithmetic at a credit union or monoline produces the same answer in this cycle, because contract-rate method also returns negative.

Falling-rate counterfactual: $300K, 5.49 per cent, 24 months remaining (Big Six)

The case where IRD actually applies. Contract 5.49 per cent, discount margin 0.50 per cent at origination, current comparison rate 3.79 per cent. Differential: 5.49 minus 3.29 = 2.20 per cent. Apply to $300K over 24 months: $300,000 × 0.022 × 24 ÷ 12 = $13,200. Floor: $300,000 × 0.0549 ÷ 12 × 3 = $4,118. Larger governs. Actual penalty: $13,200. The same file at a credit union or monoline using contract-rate method (no discount-margin reduction inflating it): $10,200, roughly $3,000 less. This is the lender-by-lender difference Big Six posted-rate methodology produces.

Source: Editorial math derivation, both methodologies cross-referenced to FCAC primary

Which Canadian lenders use which IRD methodology?

Methodology summary compiled from FCAC published guidance and lender consumer-disclosure pages. Per-lender methodology details vary; verify against your specific contract and the lender's current prepayment-charge page before acting. TD is the only row in this table backed by an explicit per-lender source quote in the verification ledger; other rows reflect industry convention as documented by FCAC.

| Lender | IRD method | Notes |

|---|---|---|

| RBC | Posted-rate | Discount-margin reduction applied. Methodology summary on RBC FAQ. |

| TD | Posted-rate | Collateral charge by default; affects switch cost more than IRD. |

| Scotiabank | Posted-rate | Some Step product variants use modified comparison. |

| BMO | Posted-rate | Methodology disclosed on request; published in standard charge terms. |

| CIBC | Posted-rate | Disclosed in renewal documentation and standard charge terms. |

| National Bank | Posted-rate | Similar to other Big Five; methodology in standard charge terms. |

Show 9 more: credit unions, monolines, and alternative lenders

| Lender | IRD method | Notes |

|---|---|---|

| Tangerine | Contract-rate | Collateral charge by default. Owned by Scotiabank but operates separately. |

| MCAP | Contract-rate | Broker-channel monoline; methodology in commitment letter. |

| MERIX Financial | Contract-rate | Broker-channel monoline. |

| First National | Contract-rate | Broker-channel monoline; one of the largest in Canada by volume. |

| Strive Capital | Contract-rate | Broker-channel monoline. Newer entrant, simpler structure. |

| Equitable Bank | Contract-rate | Schedule I bank; alt-A and prime broker channels. |

| Home Trust | Contract-rate | Alt-A specialist; check your specific product variant. |

| B2B Bank | Contract-rate | Broker-channel through Laurentian Bank. |

| Most credit unions | Contract-rate | Provincially regulated; verify with your specific credit union. |

Questions readers ask AI tools, answered

Numbers refer to late April 2026. Re-verify against linked primary sources on your decision day.

Why is the IRD penalty zero or near-zero on my 1.79 per cent mortgage?

IRD only produces a meaningful penalty when the comparison rate is materially below your contract rate, which happens in falling-rate cycles. In a rising-rate cycle, when you locked at a low rate and rates have since risen, the IRD differential is zero or negative and the three-months-interest floor governs. For files originated 2020 to 2022 at sub-2 per cent rates breaking in a 4 to 5 per cent market, the floor is the answer at every Canadian lender.

How is IRD calculated at RBC, TD, Scotia, BMO, CIBC, and National Bank?

Each Big Six bank publishes its own posted-rate IRD methodology on its consumer prepayment-charge page. The structural form compares the posted rate at the time you signed (minus the discount margin you received) against the current posted rate for a term equal to your remaining months. The discount-margin reduction tends to widen the differential when rates have fallen, producing larger penalties than contract-rate methodologies. Specific computation details vary by lender; the methodology is documented in each lender's standard charge terms.

What is the three-months-interest floor and how is it calculated?

The three-months-interest floor is the minimum prepayment penalty for a fixed-rate Canadian mortgage. Calculate it as: current balance multiplied by contract rate, divided by 12, multiplied by 3. On $400,000 at 1.79 per cent, the floor is $1,790. The floor exists so that lenders have an administrative fee threshold that does not depend on rate movements.

What should you do next?

- Phone or email your current lender and request, in writing, your current prepayment penalty if you broke today. They are required to provide the number under FCAC consumer-protection rules.

- Confirm whether your lender uses posted-rate or contract-rate methodology against the table above.

- Run the calculator with your inputs to verify the lender's quoted number is correct. If they differ by more than $50, ask the lender to walk you through the computation.

- If the penalty is the floor (rising-rate cycle), the IRD detail does not change your decision. Move on to the rate-spread and use-of-funds questions in the refinance four-question framework.

A note on whose advice to trust on this

The methodology above is sourced from lender standard charge terms and FCAC consumer-protection guidance. The math is reproducible. What I cannot give you is an authoritative quote on your specific file; only your lender can. For an independent broker review of your full file, including the IRD quote against current best-rate offers, Homewise (FSRA #12984) is a Canadian licensed brokerage that quotes multiple lenders online. RenewalRate.ca earns a commission on funded mortgages routed through Homewise.

Sources

- FCAC: Breaking your mortgage contract

- FCAC: The cost of paying off your mortgage early

- Interest Act, s. 6 (Canadian semi-annual compounding rule)

- Bank of Canada: Posted interest rates offered by chartered banks

- Ratehub: Current best Canadian mortgage rates

- Ratehub: Big bank posted and discounted rates

- Lender standard charge terms (RBC, TD, BMO, CIBC, Scotiabank, NBC, MCAP, First National, Equitable Bank). Filed in provincial land registries; available from the lender on request.

Methodology last reviewed: . How we verify every claim.