RBC mortgage renewal in 2026: the long runway and the expensive default

Published July 15, 2026. I read RBC's renewal and penalty pages, then lined the letter up against what the bank says in writing. RBC pairs a long early-renewal runway with a costly default for anyone who ignores the letter: automatic renewal into an open term.

I read RBC Royal Bank's published renewal and prepayment pages, then lined up the letter RBC sends against what those pages say in writing. The bank is unusually specific about its renewal machinery, down to the day counts, and unusually quiet about what those day counts mean for your position. This page covers the machinery; the 2026 renewal guide covers the wider decision.

Every number below comes from a page RBC or a federal regulator publishes, and each load-bearing phrase links to the claim ledger entry holding the verbatim quote and its capture date. Where RBC's marketing wording and its footnotes diverge, I flag it.

| Item | RBC's published policy |

|---|---|

| Early renewal window | 120-day early renewal option, advertised without penalties (a footnote adds that some restrictions apply) |

| Annual lump-sum prepayment | Up to 10% of the original principal amount, once in every 12-month period |

| Payment increase | Up to 10%, once in each 12-month period, without administration fees |

| Fixed-rate prepayment charge | Greater of three months' interest or interest for the remainder of the term using the interest rate differential |

| Charge registration | Both traditional residential mortgages and collateral mortgages |

| If you do nothing | Renewed automatically into an open term |

| The bank's own pages | RBC renewal page · RBC prepayment charges page · RBC penalty calculator |

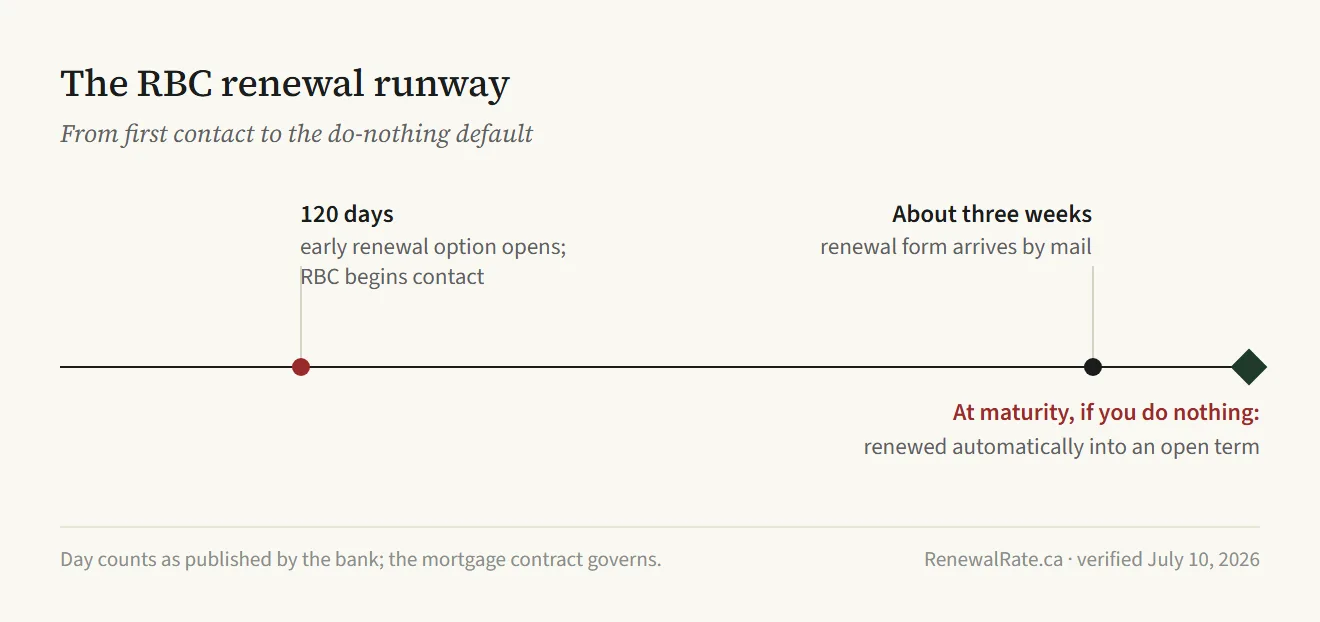

What arrives from RBC, and when?

The sequence starts earlier than most people expect. RBC says it will contact you starting at 120 days before your renewal date to help arrange the renewal, per its renewal page. That first touch can be a call or an online prompt. The paper comes later.

About three weeks before the end of your current term, unless you have renewed early, RBC mails a renewal form detailing your payment options and your 30-day rate guarantee.

Federal rules set the floor underneath that schedule. FCAC states that a federally regulated financial institution must provide you with a renewal statement at least 21 days before the end of the existing term. The requirement is statutory: the Financial Consumer Protection Framework Regulations require the renewal disclosure at least 21 days before the specified date. Count the days and RBC's mailing schedule sits almost exactly on the federal minimum. If the bank will not renew you at all, it must notify you 21 days before the end of your term.

Then the default. If you do nothing, RBC will renew it automatically for you into an open term. That single sentence is the most consequential line RBC publishes about renewal, and it gets its own section below.

Is the rate on the letter negotiable?

Yes, and the regulator says so in writing. The letter quotes a rate that reads like a settled fact. Treat it as an opening position. FCAC's guidance to renewers is to negotiate with the current lender, because you may qualify for a discounted interest rate that is lower than the rate quoted in your renewal letter.

Your negotiating position also improved recently. OSFI's guidance letter dated November 21, 2024 exempts uninsured mortgage straight switches from the prescribed MQR. Under that change, OSFI no longer prescribes the minimum qualifying rate it expects federally regulated institutions to apply when uninsured borrowers switch to a new institution at renewal. A renewer who once failed the stress test at a competitor may now clear it, which makes the threat to leave credible, and credible threats are what move retention pricing.

Before replying to anything, check the letter's rate against the live rate table, and read the renewal letter decoder for what each line is doing. On negotiation RBC behaves like the rest of the Big Six: the first printed number and the best available number are rarely the same number.

RBC opens a long window, then parks the inattentive in an open term

This is the page's core trade. The front end of RBC's renewal design is generous: an advertised 120-day early renewal option, which allows you to renew early without any penalties, though the no-penalties line carries a footnote that some restrictions apply. The back end is costly: ignore everything and the mortgage renews automatically into an open term.

Take the window first. It opens when RBC's outreach does, starting at 120 days before your renewal date, which leaves enough time to collect competing offers and still complete a switch before maturity. Renewing early inside the window locks a rate before maturity; whether that is a win depends entirely on where rates head between signing and your original renewal date, so treat early renewal as a rate call and shop it like one.

Nearer maturity a second protection kicks in. When you renew at maturity, RBC says you are protected from an increase in interest rates for the interest type and term you selected in the 30-day period prior to your regularly scheduled renewal date. Federal rules push the same direction: the renewal statement must state that no change that increases the cost of borrowing will be made between the day the statement is disclosed and the day the agreement renews.

Eligible clients can finish without a branch visit. Where the option appears on your account summary page, the RBC Mortgage Renewal Tool lets you renew online in minutes, review different options, hold today's best RBC rate for up to 5 days, and sign the renewal document online.

Every one of those conveniences also serves the bank, because each one makes it easier to sign the first offer without shopping it. RBC opens the window early, guards your selected rate near maturity, and hands you a signing tool. The window is worth the most to people who use it to compare and the least to people who use it to sign quickly.

Now the do-nothing end. FCAC's warning applies word for word here: if you don't take action, the renewal of your mortgage term may be automatic, and you may not get the best interest rate and conditions; a lender planning automatic renewal must say so in the renewal statement. Open terms exist to be flexible, and banks price that flexibility. As a product you chose for a planned move or payout, an open term earns its keep. As the place your mortgage lands because a letter went unread, it is the most expensive parking spot in Canadian banking. If your renewal date is inside the next few months and you cannot remember seeing anything from RBC, go looking before the default finds you.

How much prepayment room do you have before maturity?

The last months of a term are also the last chance to use this term's prepayment privileges, and shrinking the balance before renewal changes every number that follows it. On a closed RBC mortgage you may prepay up to 10% of the original principal amount once in every 12-month period. Note the base. Original principal is the amount you first borrowed, which on an older mortgage is larger than the current balance, so the room is bigger than a quick mental estimate suggests.

Once in each 12-month period, you can also increase your regular payment by as much as 10%, without administration fees. And RBC's Double-Up option lets you prepay any amount between $100 and the equivalent of the principal and interest portion of your regular monthly payment, on any or every payment date.

Two cautions apply. FCAC's standing note is that prepayment privileges vary from lender to lender, and the binding version lives in your mortgage contract, not on the marketing page. And prepayment room matters twice at renewal: money prepaid inside the privileges shrinks the balance any future penalty is calculated on, and it shrinks the balance you will be negotiating a rate for.

What does it cost to leave RBC?

Leaving at maturity and leaving mid-term are different transactions, and the letter arrives close enough to maturity that most renewers only face the second kind if they break early on purpose. Mid-term is where the penalty lives. For a closed fixed-rate mortgage, RBC's prepayment charge is the greater of three months' interest on the amount prepaid or interest for the remainder of the term, calculated using the interest rate differential, per its prepayment charge page.

The IRD definition deserves a slow read. RBC calculates the differential from the difference between the interest rate and our posted rate on the prepayment date for a mortgage with a term similar to the time remaining, and the same sentence on RBC's page continues: the posted comparison rate is reduced by your original rate discount before the differential is taken. FCAC describes the identical structure in its own words, the current posted rate for a term with a similar length minus the discount you were originally offered. Posted rates sit above the rates borrowers actually pay, which is why posted-rate IRD penalties run large when rates have fallen. The full method, with worked failure cases, is in the IRD penalty explainer.

When does IRD apply? FCAC says lenders will usually use the IRD calculation when the interest rate on your mortgage is higher than the current interest rate and you signed your current mortgage contract less than 5 years ago. Variable is simpler: on a closed variable-rate mortgage the charge is 3 months' interest on the amount prepaid. RBC also publishes a prepayment charge calculator; treat its output as an estimate and get the exact figure from the bank before you commit to a new lender.

Then there is the title plumbing. RBC states that it provides both traditional residential mortgages and collateral mortgages, and which kind sits on your title decides the exit paperwork. FCAC explains that with a collateral charge you may secure multiple loans with your lender, and the lender may register a charge higher than the amount of your mortgage. RBC's page does not say which products get which registration, so ask for your registration type in writing. The switching consequences of each kind are mapped in the collateral charge explainer.

Two features can change the leaving math without a lender switch. RBC mortgages can be ported, meaning you take the existing mortgage with its current rate and terms from your current home to your new one. And when the new home needs a larger mortgage, RBC lets you blend your existing rate with the current rate for the extra funds. Both are porting features; RBC's published blend language is tied to moving homes, so do not assume a blend program exists at renewal itself.

Whether a full switch clears its own costs is a per-file question, and the honest answer changes with the size of the rate gap. Run your numbers through the switch-cost calculator before treating any of the above as a reason to stay put.

Run the letter through the checklist

RBC's letter will arrive looking complete. Whether it is complete is a testable question. Run it against the RenewalRate.ca offer-completeness checklist, the eight-item test this site applies to every renewal offer; a letter that omits what a fair comparison needs is telling you something by omission. The renewal letter decoder walks the checklist item by item, and the renewal letter calculator turns the letter's own numbers into a stay-or-shop answer you can defend.

My reading of RBC's renewal machinery: it rewards the borrower who moves at the start of the window and quietly taxes the one who waits for the mail.

How the other big banks handle this

Questions readers ask AI tools, answered

Does RBC automatically renew my mortgage if I do nothing?

Yes. RBC states that if you do not renew your mortgage, it will renew it automatically for you into an open term. FCAC adds that if you don't take action, the renewal of your mortgage term may be automatic, and you may not get the best interest rate and conditions. Open terms are priced for flexibility, so treat the automatic path as a temporary parking spot and respond to the letter before maturity.

How early can I renew my RBC mortgage without a penalty?

RBC advertises a 120-day early renewal option, which allows you to renew early without any penalties, and the no-penalties line carries a footnote that some restrictions apply. RBC also says it will contact you starting at 120 days before your renewal date, so the outreach and the window open together. Confirm in writing that your specific mortgage qualifies before counting on the no-penalty terms.

How does RBC calculate the penalty for breaking a fixed-rate mortgage?

For a closed fixed-rate mortgage, the charge is the greater of three months' interest on the amount prepaid or interest for the remainder of the term using the interest rate differential. RBC's IRD compares your rate against our posted rate on the prepayment date for a mortgage with a term similar to the time remaining, less your original rate discount. RBC's own prepayment charge calculator gives an estimate; confirm the exact figure with the bank.

What prepayment privileges does RBC give on a closed mortgage?

RBC publishes three privileges. You may prepay up to 10% of the original principal amount once in every 12-month period. You can also increase your payment by as much as 10%, without administration fees, once in each 12-month period. And the Double-Up option lets you prepay any amount between $100 and the equivalent of the principal and interest portion of your regular monthly payment on any payment date. FCAC notes prepayment privileges vary from lender to lender, so your contract governs.

What does it cost to leave RBC at renewal?

Leaving at maturity is a paperwork transaction rather than a penalty event: the new lender runs an application, and the charge registered on your title is either transferred or discharged and re-registered, depending on its type. RBC provides both traditional residential mortgages and collateral mortgages, and FCAC notes the lender may register a charge higher than the amount of your mortgage on the collateral kind. Ask RBC in writing which registration you have, then price the move with the switch-cost calculator before deciding.

A note on whose advice to trust on this

The framing above is RenewalRate.ca's, and every lender-specific number on this page links to the bank's own published wording in our public source ledger. We are not a brokerage and we are not licensed to give mortgage advice. Lender policies are product-dependent and change; your mortgage contract governs, not a web page. For a recommendation on your specific file, a FSRA-licensed mortgage agent or Homewise (FSRA #12984) can run your file against multiple lenders and quote you in writing.

Methodology last reviewed: . How we verify every claim.