Scotiabank mortgage renewal in 2026: what the letter says and what the STEP umbrella means

Published July 15, 2026. I read Scotiabank's renewal pages, its penalty disclosure PDF and its STEP brochure so you would not have to. The letter is the easy part. Whether your mortgage sits under the Scotia Total Equity Plan umbrella decides how much work, and how much money, leaving would actually take.

I read Scotiabank's renewal hub, its Advice+ guidance, the prepayment-charge disclosure PDF, the Scotia Total Equity Plan page, and a brochure on charge types that has been quietly living on scotiabank.com for years. Scotiabank documents its renewal mechanics more thoroughly than most banks. It just spreads the documentation across several pages, and the letter that lands in your mailbox summarizes almost none of it.

This page is the assembly job. Every lender number below links to a verified entry in the public ledger, most of them from Scotiabank's own pages, the rest from FCAC and federal regulation. The rate on the letter is one question. The more expensive question, for a large share of Scotiabank borrowers, is what the mortgage is plugged into: the STEP umbrella decides how much work leaving would actually take.

| Item | Scotiabank's published policy |

|---|---|

| Early renewal window | Up to 6 months before the mortgage expires |

| Annual lump-sum prepayment | 10%, 15% or 20% of the original principal amount, depending on product |

| Payment increase | Match-a-Payment: double a regular payment on any regular payment date, no fee |

| Fixed-rate prepayment charge | Greater of 3 months interest or the Interest Rate Differential |

| Charge registration | Two charge types: collateral or conventional |

| If you do nothing | Automatically renewed into a 6-month fixed rate closed term |

| The bank's own pages | Scotiabank renewal page · Scotiabank prepayment charges page · Scotiabank penalty calculator |

What arrives from Scotiabank, and when

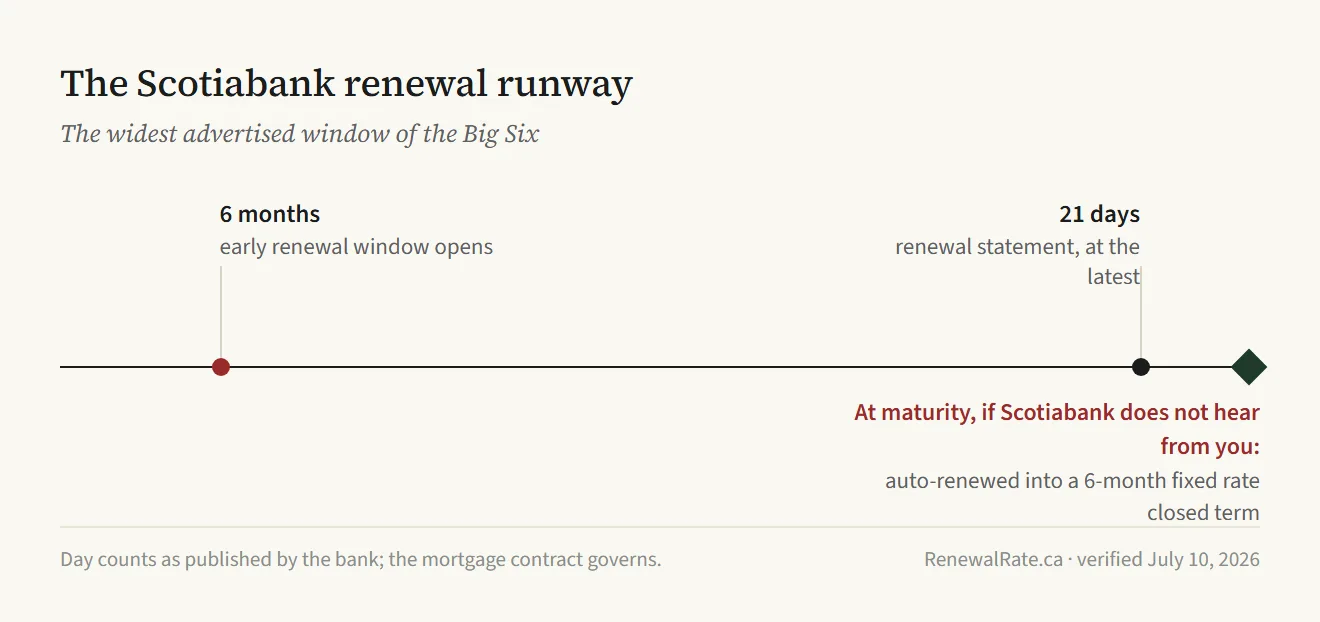

Scotiabank's renewal guidance tells borrowers to expect the renewal statement at least 21 days before the end of your existing mortgage term. That timing is not a courtesy. FCAC requires every federally regulated financial institution to provide the statement at least 21 days before the end of the existing term, and the Financial Consumer Protection Framework Regulations carry the same deadline as prescribed disclosure.

The paper itself tends to move earlier than the floor. Scotiabank's notice during the Canada Post disruption told clients who had not received their Mortgage Renewal Agreement 30 days before your mortgage maturity date to visit their closest branch for a copy, which tells you when the bank itself expects the document to be in your hands.

The statement also freezes the offer in your favour. The statutory disclosure must include a statement that no change that increases the cost of borrowing will be made between the day the statement is disclosed and the day the agreement renews. The rate on the letter can drop before your maturity date. By the bank's own disclosed statement, it cannot rise.

If you do nothing, Scotiabank does something. The same postal-disruption notice states that if the bank does not hear from you before your maturity date, your mortgage will be automatically renewed into a 6-month fixed rate closed term. FCAC's warning is conditional on exactly this: take no action and the renewal of your mortgage term may be automatic, meaning you may not get the best interest rate and conditions. Auto-renewal is a convenience for the bank and a holding pattern for you, at a term nobody picks on purpose. In the rarer case where the bank walks away, FCAC says the lender must notify you 21 days before the end of your term if it will not renew.

The full timeline, from first contact to maturity day, is laid out in the 2026 renewal guide. This page stays on what Scotiabank specifically does.

The rate on the letter is an opening number

Scotiabank, like every large Canadian lender, maintains posted rates and offers discounts off them. The letter usually quotes something between the two, and it is rarely the bank's final position. FCAC's guidance is unusually blunt for a regulator: negotiate with your current lender, because you may qualify for a discounted interest rate that is lower than the rate quoted in your renewal letter. The agency that supervises Scotiabank is telling you, in writing, that the letter's number is negotiable.

The friction-free option works against you here. On its renewal page, Scotiabank promotes the ability to renew online in minutes after exploring your options. The convenience is real. It is also the mechanism by which a bank collects signatures at the letter's rate from people who never asked whether that rate was the best one on offer. Before clicking anything, put the letter beside the current market table and read what each line of the letter commits you to.

The STEP umbrella is the real subject of your renewal

The Scotia Total Equity Plan is Scotiabank's borrowing umbrella: a mortgage and additional credit products secured under a single registration against the home. Under STEP you can initially borrow up to 80% of the value of your home, including up to 65% for line of credit products. If a Scotiabank advisor ever mentioned adding a line of credit later without new paperwork, you are probably in one.

The registration type is what matters at renewal. Scotiabank offers two types of mortgage charges, collateral or conventional, and STEP runs on the collateral kind. FCAC's description of a collateral charge explains the design: you may secure multiple loans with your lender, and the lender may register a charge higher than the amount of your mortgage. What that structure costs across lenders is covered in the collateral charge explainer. The Scotiabank-specific consequence is the umbrella itself.

Renewing inside STEP is deliberately easy. The mortgage component renews, the umbrella stays up, nothing gets re-registered. Leaving is a different operation. Collateral charges generally cannot be transferred between lenders; leaving means everything secured under the charge is paid out or moved before the charge comes off title, and the receiving lender then registers its own. A competing lender that wants your mortgage has to take on the whole umbrella.

Scotiabank's own brochure states the sharpest version of this. If you hold a STEP product and wish to register a second charge, Scotiabank will request you to close your STEP. Read that in a renewal context: the umbrella does not co-exist with another lender's security on your title. Want a second mortgage or any other charge sitting behind Scotiabank's? The bank's published answer is to wind up the plan first.

None of this makes STEP a bad product. Umbrella structures like it exist at other Big Six banks under different names, and the lender index compares how each behaves at renewal. What STEP does is turn your renewal from a rate decision into a structural one. The rate gap a competing lender must clear is the same as anyone's. The work that gap must justify is larger, and Scotiabank knows that when it prices your letter.

Your prepayment room before maturity

Scotiabank's prepayment privileges depend on which mortgage you chose at signing. Depending on the options selected, you can repay up to 10%, 15% or 20% of the original principal amount of your mortgage at any time during each year of the term. On top of the lump-sum room, eligible borrowers get Match-a-Payment, which allows you to double your current mortgage payment of principal and interest on any regular payment date without a fee or prepayment charge.

Which tier you actually hold is a contract question, not a website question. FCAC's baseline advice applies here: prepayment privileges vary from lender to lender, so check your own mortgage contract rather than any bank's marketing page. Even Scotiabank's own prepayment calculator hedges, noting that for partial prepayments it applies a standard prepayment allowance of 15% of the original principal balance of your mortgage per year as a working assumption rather than your contractual figure.

Then there is the early-renewal window, where Scotiabank genuinely stands out. You can renew your mortgage up to 6 months before it expires. That is the widest early-renewal window published by any of the Big Six. Put on a calendar: Scotiabank's window has already been open for around two months by the time most other banks' windows open at all.

What the window is for: locking a rate early when you expect rates to rise, or starting the negotiation clock while you still have months of runway to collect competing offers. It is also the calmest moment to rethink term length and payment schedule, well before the letter's deadline pressure arrives.

What it costs to leave Scotiabank

Leave on your maturity date and no prepayment charge applies; the cost of the move is the discharge and re-registration work described above, which the switch-cost calculator prices for any specific file. Leave before maturity and Scotiabank's disclosure document governs: for fixed rate mortgages, the typical charge to pay out early is the greater of 3 months interest or Interest Rate Differential.

The IRD is where method matters. Scotiabank defines its comparison rate as the current posted interest rate offered by us for a new fixed rate closed term mortgage with a term that is closest to the remaining term of your existing mortgage. Before the comparison runs, the Current Interest Rate will be discounted by any rate discount you received on your existing mortgage. That pairing, posted rate minus your original discount, is the construction that tends to produce the large IRD figures borrowers report from the big banks. My full walkthrough of the method is in the IRD explainer.

FCAC's consumer pages describe the same architecture from the outside. The penalty will usually be the higher of an amount equal to 3 months' interest on what you still owe or the interest rate differential. Lenders usually reach for the IRD calculation when your rate is above current rates and you signed your current mortgage contract less than 5 years ago. FCAC's own list of IRD inputs includes the current posted rate for a term with a similar length minus the discount you were originally offered, which is the Scotiabank method almost word for word.

Do not estimate any of this by hand. Federally regulated financial institutions, like banks, have a prepayment penalty calculator on their website, and Scotiabank's is linked from the ledger entry above. Run it before you sign anything, then weigh the output against the rate gap you are chasing.

One obstacle to leaving disappeared recently. OSFI's guidance letter dated November 21, 2024 exempted uninsured straight switches from the stress test's prescribed floor. In its words, OSFI will no longer prescribe the minimum qualifying rate (MQR) that it expects federally regulated financial institutions to apply when uninsured mortgage borrowers switch to a new institution at renewal. If requalification anxiety kept you renewing by default, the rule that fed it is gone for straight switches.

Short of paying the charge, the closed mortgage schedule offers side doors. It contains a portability provision: holders of a closed fixed rate mortgage may transfer your existing mortgage loan balance and the remaining term to a new home. When you need more money mid-term, the same schedule permits combining the existing balance with new funds, where the interest rate on the new loan will be a blending of the rate you were paying and the rate for the extended term. Both keep you at Scotiabank, which is of course the point of offering them.

Before you sign, run the offer-completeness checklist

Every renewal letter reviewed on this site goes through the RenewalRate.ca offer-completeness checklist, an eight-item test of whether the letter gives you enough information to compare it against the market at all. The checklist's usual failure points are the things no letter volunteers: what leaving costs, and what structures sit behind the offer. On a STEP file, both live outside the letter, in the plan documents and the charge on your title. Work through the letter guide with your statement in hand, then put the numbers into the renewal letter calculator to see what the offer costs over the term you would be signing.

If the letter clears the checklist and the rate clears the market, renew and get on with your life. If either one fails, everything above came from Scotiabank's own documents, and the window to act on it opens earlier than most borrowers assume.

How the other big banks handle this

Questions readers ask AI tools, answered

Does Scotiabank automatically renew my mortgage if I do nothing?

Yes. Scotiabank states that if it does not hear from you before your maturity date, your mortgage will be automatically renewed into a 6-month fixed rate closed term. FCAC warns that when renewal is automatic you may not get the best interest rate and conditions, and a lender planning to auto-renew must say so in the renewal statement. Treat auto-renewal as a fallback and respond to the letter before maturity.

How early can I renew my Scotiabank mortgage before it matures?

Scotiabank lets you renew your mortgage up to 6 months before it expires, the widest published early-renewal window among the Big Six banks. The renewal statement itself must still arrive at least 21 days before the end of your existing mortgage term. Use the gap between those dates to negotiate: the earlier you engage, the more runway you have to collect competing offers and pressure-test the letter's rate.

How does Scotiabank calculate the penalty for breaking a fixed-rate mortgage?

For fixed rate mortgages, the typical charge is the greater of 3 months interest or Interest Rate Differential. The IRD comparison uses the current posted interest rate for a new fixed rate closed term mortgage with a term closest to the remaining term, and that rate is discounted by any rate discount you received on your existing mortgage. Posted minus your original discount tends to widen the differential, which is why Scotiabank IRD figures surprise people. Run the bank's own calculator before deciding anything.

What happens to my Scotia Total Equity Plan (STEP) if I switch lenders at renewal?

STEP runs on a collateral charge; FCAC explains that this structure lets you secure multiple loans with your lender, registered for more than the mortgage itself. Leaving means every product under the umbrella has to be paid out or moved before the collateral charge comes off title, after which the new lender registers its own charge. Scotiabank's brochure is explicit on a related point: wish to register a second charge and Scotiabank will request you to close your STEP. None of this is impossible. It is simply more work than moving a stand-alone mortgage.

How much extra can I pay on my Scotiabank mortgage each year without a penalty?

Depending on the options selected for your mortgage, you can repay up to 10%, 15% or 20% of the original principal amount at any time during each year of the term. Eligible borrowers can also use Match-a-Payment to double your current mortgage payment of principal and interest on any regular payment date with no fee. Check your own contract for the exact tier: Scotiabank's calculator applies a standard prepayment allowance of 15% as an assumption, not a guarantee.

A note on whose advice to trust on this

The framing above is RenewalRate.ca's, and every lender-specific number on this page links to the bank's own published wording in our public source ledger. We are not a brokerage and we are not licensed to give mortgage advice. Lender policies are product-dependent and change; your mortgage contract governs, not a web page. For a recommendation on your specific file, a FSRA-licensed mortgage agent or Homewise (FSRA #12984) can run your file against multiple lenders and quote you in writing.

Methodology last reviewed: . How we verify every claim.